Since 2018, I had been on a mission to secure the best child medical insurance for my toddler son. I felt relieved when I finally signed up for a medical plan for my son in 2020.

In this post, I will be sharing the whole process of how I chose the best child medical insurance for my son.

Table of Contents

- The process of choosing the best child medical insurance for my son

- The coverage details of my child’s medical insurance

- Why did I choose an investment-linked plan instead of a standalone medical plan?

- Why do I only buy medical insurance now?

- Personal tips to get the best child medical insurance at a lower premium

- 1. Consider a standalone medical plan

- 2. Consider a family Takaful plan

- 3. Tweak the coverage details

- 4. Consider a lower hospital and surgical benefits plan

- 5. Get medical insurance when the child is 6 years old and above

- 6. Get multiple quotations from different agents

- 7. Choose a good insurance agent

- Other things worth taking note

- Final thoughts

[Disclosure: This page may contain affiliate links. I may receive a small commission when you click on those links, but it will not cost your anything extra. I only recommend services I use now, have used in the past, or would use if there was a personal need.]

The process of choosing the best child medical insurance for my son

Compared to getting medical insurance for myself and my husband, getting a medical plan for my son was not that simple.

Prior to taking up the policy, I spent a lot of time reading and digesting as much information as possible on insurance coverage.

I know I can just ask the insurance agent, but I’ve learned not to fully rely on the insurance agent. So, I told myself, I must brush up on my insurance knowledge.

Thus, I was more aware of the options I have. This also means more comparison and considerations involved.

Below were the steps I took to get the best child medical insurance for my son.

1. Improve my knowledge of medical insurance for children

Firstly, as mentioned above, I took the time to learn as much as possible about insurance. Especially on medical insurance for children and general insurance protection for juniors.

For the first time, I also spent time reading my hubby’s and my insurance policies.

Along the process, I discovered valuable insurance knowledge such as:

- important insurance terms that guided me to make better insurance decisions.

- comparison between a standalone medical plan and a rider attached to the main policy such as an investment-linked plan.

- 5 strong reasons why one should not depend on employer insurance coverage.

- tips on how to lower health insurance premiums.

- 6 don’ts with medical and health insurance.

I find that having some insurance knowledge, it’s easier for me to understand medical insurance quotations. Besides, when the agents knew that I know about insurance matters, they were less pushy.

And I can tell that the insurance agents are more careful with their proposals and explanation.

2. Gather the information on the local medical center

Secondly, I gathered the room rates for the medical canters in Kuching. What I did was:

- I checked their room rates from their official website.

- I made a call to the medical centers asking for their recent room rates.

So that I can have a clear picture of the budget for the hospital room rates around the Kuching area.

Based on this information, I found out that the hospital room rates in Kuching (in 2020) range from RM65 (3 bedded) to RM450 (deluxe room).

Then, I also found out that MyPF has compiled a list of Malaysian Hospitals Room Rates. Although some medical centers are not on the list, it does provide a very good guideline for hospital room rates in Malaysia.

3. List down my requirements

Thirdly, I sat down and listed my requirements, features, and other considerations related to my son’s medical plan.

Among those on my list:

- Affordable budget

- I budgeted RM150 for my son’s medical coverage

- The coverage meets our current needs and future needs (for the next 20 years)

- cover hospitalization and surgeryoutpatient treatmentshospital benefits

- critical illness

- personal accident

- waiver of premium

- some sort of savings or investment

- My requirement and features

- high annual limit

- no lifetime limit

- sufficient room and board charges

- list of panel hospitals including my preferred medical centers

- cashless admission

- co-payment policy for a lower premium

- Choosing between a standalone or as a rider of an Investment-linked plan

- Reasonable coverage term

- Buy online or through an insurance agency

- Convertible to the adult plan

- Additional requirements and features

- payor benefits

- The insurer must be a PIDM insurer member

Then, I started to prioritize the list according to our needs.

4. The procedure when choosing the best child medical insurance plan for my son

Next would be the procedure involved when I was choosing the best child medical insurance plan for my son.

a. Gathering medical insurance quotations

Once I knew what I want for my son’s medical insurance plan, I started to ask for quotations from:

- my existing insurance agents

- insurance agents who had approached me before

- insurance provider via online

I learned that it’s a good idea to get quotations from:

- a different agent from a different insurer

- a different agent from the same insurer

Because I got to see different ways of presentation of information. Some were more detailed while some just provided brief answers to my questions.

In most cases, the insurance agents wanted to meet up. But, to gather the quotations, I told them to just send them to my email.

When asking for quotations, I provided them with my requirements as below:

- my budget of RM150

- tips: tell the insurance agent a slightly lower than your actual budget. Because most likely, they’ll send you a quotation with a slightly higher premium.

- priority is given to health and medical coverage

- minimal total sum assured

- minimal savings or investment

- must include payor benefit

- so that in case something unfortunate happens to me, my son’s policy premiums are waived.

As expected, some agents only sent me a single quotation for my consideration. The most I received were two quotations.

Surprisingly, I encountered an agent who told me his system can’t generate a proposal based on a premium of RM150. Funny, right? So, I just move on to other agents.

The point here is that the more quotations, the more options I have. And I got to learn new things, new terms, and new experiences.

b. Study the quotations

Once I received the quotations, I sat down and did a comparison.

It took me a few weeks to really study and do the comparison.

I found out that, for the same premium amount, the features and coverage benefits were more or less the same.

c. Finalizing quotations

From all the quotations, then I chose one that fit my requirements. Also, most importantly, the quotation came from a reliable insurance agent who meets my criteria for a good insurance agent.

Once I felt comfortable with the plan and the insurance agent, I asked the agent to tweak and adjust the quotation according to my preferences as below:

- Medium-range hospital benefits with high annual limits

- Minimal death/Total Permanent Disability (TPD) coverage

- Minimal critical illness coverage

- Medium personal accident benefits

- Payor benefits

When finalizing, I would recommend meeting up with the short-listed agents. Because when meeting face-to-face, you’ll roughly know if you feel comfortable with the agent.

d. Asking questions related to the quotations

While finalizing the quotations, I also prepared a list of questions about the medical plan.

Below were the questions I emailed my preferred insurance agent:

- If the hospital Room and Board amount exceed the amount allocated for the plan, how are the charges?

- Does the plan come with a physical card or an e-medical card?

- Is it a cashless admission plan or through claim and reimbursement?

- Does the claim inclusive of diagnoses such as X-ray, MRI scans, or other imaging?

- Are take-home drugs covered?

- Why some of the well-known medical centers in Kuching are not listed under the panel hospital?

The insurance agent took some time to reply to my email. Since it’s through email, I guessed she just wants to make sure she provides the right answer.

According to her, most of her customers asked her verbally. This means not many customers like me asked through email.

5. Enrollment process

Once my husband and I were happy with the quotation, we proceed with the enrollment.

Actually, I had planned to meet up with the agent in the middle of March 2020 but then it was Movement Control Order (MCO). So, we postponed the meeting.

After a few follow-up messages from the agent, towards the end of July 2020, we decided to take up the plan.

The enrollment process is as below:

i. Video meeting session

Due to the pandemic, we scheduled a video meeting together with my son. This was where the insurance agent explained the policy in detail and asked important questions such as health history.

The video meeting lasted for about one hour.

ii. Submission of supporting documents

After the video meeting session, I started to prepare and submit the supporting documents as below:

- My son’s details

- NRIC

- heights

- weights

- home address

- Parents’ details

- heights

- weights

- home address

- company name

- company address

- smoking or non-smoking

- alcohol consumption

- occupation

- mobile phone number

- email address

- bank account details

- a recent selfie holding NRIC

iii. Received proposal form from the insurer

The next day, I received an email from the insurer to confirm my application. I replied accordingly.

A few hours later, I received an acknowledgment email informing me the application was already in process.

This is followed by an SMS with the instruction for the first payment. Once I made the payment, a few hours later, I received a payment acknowledgment receipt through email.

iv. Received e-policy

One week later, I received the e-policy from the insurer.

I was not very happy with the e-policy. So, I called up my agent and requested a hardcopy policy instead.

She’s kind enough to help to print out the e-policy so that I can read through the policy during the 15 days Free Look period.

Finally, in December 2020, I received my son’s insurance policy.

Previously, for all my husband’s and my insurance policies, the insurance agents sent us the printed policy by hand within weeks of signing up for the plan.

In my opinion, the insurer should consider it for the long term and as a service to their customer. When an emergency happens, they can’t expect the policyholder to patiently search the e-policy through her email, right?

An insurance policy is such an important document. Thus, the insurer should provide their customer with a properly printed insurance policy and not just an e-policy.

The coverage details of my child’s medical insurance

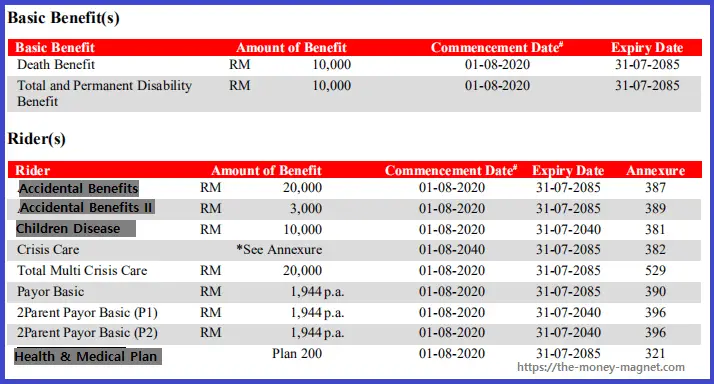

Here are some of the important details of my son’s medical insurance plan:

- Type of plan: Investment-Linked Plan

- Monthly premium: RM191

- Protection term: 65 years

- Basic Sum assured: RM10,000

- Total and Permanent Disability Benefits: RM10,000

- Medical Benefits: Room and board up to RM200 per day with a maximum of 120 days per year

- Overall annual limit: RM1,380,000

- No lifetime limit

- Copayment: RM300 per disability

- Child Specified Illness: RM10,000

- Critical Illness Benefits: RM10,000

- Accidental Benefits: RM20,000

- Investment Premium Riders: RM348 per year

- Double Payor Benefits

And below is a print screen of the summary of my son’s medical insurance policy attached to an investment-linked plan.

Do take note, that I purposely replaced the name of the riders with a general name because I do not wish to influence you with these riders.

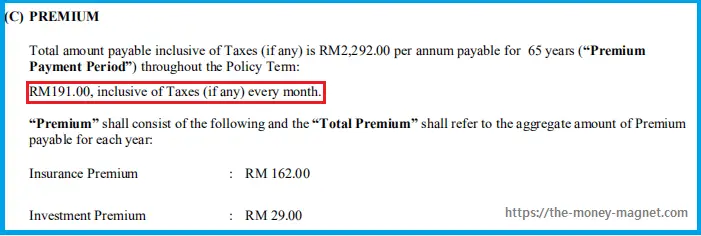

Below is the print screen of the monthly premium stated in my son’s policy.

There are some other less important benefits that I didn’t share here.

Why did I choose an investment-linked plan instead of a standalone medical plan?

Even though I can save about 50% on the monthly premium if I signed up for a standalone medical plan for my son, I am still enrolled in an investment-linked plan.

These are the reasons:

1. I want the payor benefits

In my opinion, I believe the payor benefits rider is a crucial part of my son’s medical insurance plan. Because compared to others, we started our parenthood quite late.

In case anything unfortunate happens to either my husband or me, my son’s coverage is not affected (valid until my son reaches 25 years old).

Since standalone medical insurance does not offer this benefit, my only choice is an investment-linked plan.

2. I want to secure a medical plan for my child

Although a standalone plan can offer a much lower premium, I am concerned about the guaranteed renewal terms.

But, with an investment-linked plan, I can secure a medical plan for my child without worrying about the guaranteed renewal terms.

Furthermore, I foresee a few years down the road, for the same medical benefits, the premium might be much higher due to the rising medical cost in Malaysia.

Thus, I should secure a medical plan for my son as soon as possible.

3. A more complete insurance plan

Other than medical insurance, I also foresee I’ll need to take up other coverage such as:

- critical illness

- personal accident

Instead of getting them separately from other insurers, might as well I added these as riders to the investment-linked plan under one policy.

Maybe some of you might think that young kids do not need to have an insurance plan. But in my opinion, young kids nowadays also need to have insurance coverage.

I shared the 7 reasons why I signed up for an insurance plan for my son in another post: Should I buy an insurance plan for my kid?

4. Flexibility to adjust insurance coverage

Compared to a standalone plan, an investment-linked plan offer greater flexibility to adjust the insurance coverage.

For that, I can adjust the insurance coverage based on our needs and affordability.

If you are considering investment-linked coverage for your child, take a look at Prudential’s PRUMy Child Plus. The plan offers protection for both mummy and baby from as early as 13 weeks of pregnancy.

Why do I only buy medical insurance now?

Perhaps, you are wondering why only now I took up medical insurance coverage for my son. Why not earlier or later?

These are the reasons:

1. Previously was under employee benefits

Firstly, before I left my full-time employment in mid-2018, my family and I were covered under my previous employer’s group insurance benefits.

The coverage was quite good. So, I didn’t bother to look for a medical plan for my son.

2. Lower premium for kids aged 4 onwards

Secondly, based on the research I did on medical insurance coverage for children, I learned that the insurance premium started reducing from the age of 4 onwards.

The reason is that newborns, infants and toddlers below 4 years old have higher risks of getting admitted to hospitals.

From the quotations I received, I can confirm that for the same benefits, there’s a premium difference between a 3-year-old and a 4-year-old.The

For the same benefits, the insurance premium for a 4-year- old is RM191.00.

Actually, from some of the online insurance premium schedules, you’ll also see a pattern where the monthly premium starts to go down after the child is 4 years old.

Anyway, I was taking a risk by not having a medical insurance plan for my son for the two years I left my employment.

3. Avoid higher premiums as my age increases

Then, you might ask me why I didn’t wait until my son is a bit older, say 7-year-old (the premium for a 7-year-old can be much lower than RM191.00 per month).

Well, I can’t wait any longer because my age and my husband’s age are catching up. As our ages increase, we have higher risks. So, the insurance premium will be higher.

Thus, from my calculation, the best time to get a medical plan for my son is when he is 4 years old.

4. Get a medical plan while everything is ok

When I requested medical plan quotations for my sons, the two commonly asked questions from insurance agents were:

- “Does your son has a medical history?”

- “Does your son ever admit to the hospital?”

The reason behind this is that these insurance agents want to know whether their potential clients are healthy or with pre-existing illnesses.

For prospects with pre-existing illnesses, there are additional terms and conditions set by the insurer’s underwriting team. If the risks are too high, the insurer has the right to reject the application.

This is why I decided to get the best child medical insurance when everything is ok.

Personal tips to get the best child medical insurance at a lower premium

As parents, my husband and I want the best for our son, including giving him the best child medical insurance plan. But we know the best child medical insurance plan usually comes with a hefty premium.

So, for the past years, I did a lot of reading on insurance, especially medical insurance plans for kids. From the intensive reading, I’ve learned a few tips to have child medical insurance at a lower premium.

Here are some of my personal tips:

1. Consider a standalone medical plan

Compared with an investment-linked plan, a standalone medical plan can save about 50% of the monthly premium. That’s quite a lot of savings.

But do be aware of the potential risks of having a standalone medical plan. Such as:

- guarantee renewal clause

- meaning if the policyholder made a huge medical claim, will the insurer renew his/her policy for the next year and the years to come?

- if the insurer agrees to renewal, is there an individual premium loading that causes a huge premium hike?

- limited health and medical coverage

- do have a backup plan just in case the unfortunate happens and the coverage is not sufficient.

Before deciding on a standalone medical plan, probably it is best to get a written confirmation on the guarantee renewal clause from the insurer.

This is an important step to make sure the insurer continues to provide medical coverage, especially at the time you need the coverage the most.

Other than the above 2 main potential drawbacks of having a standalone medical insurance plan, I also share other pros and cons of a standalone medical plan in another post, Standalone Versus Investment-linked Plan (for medical insurance).

Nevertheless, having a standalone medical plan is better than having no medical plan at all.

2. Consider a family Takaful plan

I’ve read that, generally, a family Takaful protection plan (protection plan based on the concepts of Shariah) can be much lower than a family insurance plan.

I didn’t explore further on family Takaful plan because:

- both my husband and I have our own medical insurance plan

- all my insurance agents only send me family insurance plans

So, if possible, do ask for family Takaful quotations from your insurance agents or insurance provider for consideration.

3. Tweak the coverage details

This is how I managed to reduce my son’s medical insurance premium, by tweaking the coverage details. Such as:

- minimal basic sum assured

- only add the important riders to an investment-linked plan

- shorter coverage term

One important thing, with all the tweaking, I must be aware of all the risks I am taking.

4. Consider a lower hospital and surgical benefits plan

Usually, hospital and surgical benefits come in three plans: lowest, medium, and highest. Opting for a lower hospital and surgical benefits plan definitely helps to reduce the medical premium.

Before deciding, do check out the average room and board rates. Also, get confirmation from your agent or insurer about what will happen if the room and board rates exceed the limit offered by the medical plan.

Whatever the decision, just make sure you are aware of all the risks you are taking.

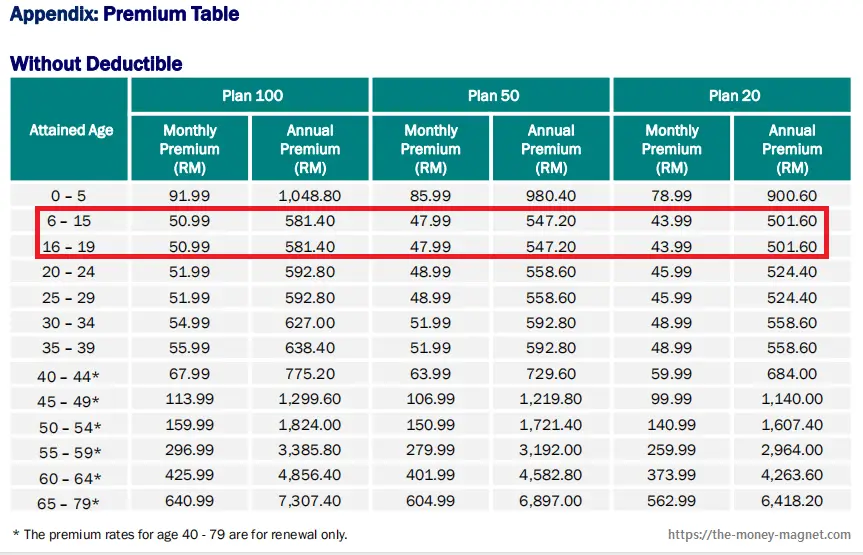

5. Get medical insurance when the child is 6 years old and above

By referring to the many quotations I received both online and offline, I’ve learned that the premium for child medical insurance is much lower after the child is 6 years old.

Let me share an example of a factsheet from the online quotation I received from the AXA e-medic plan below:

As shown above, there’s about a 40% difference in premium for a child below 6 years old and above 6 years old.

But then one must be aware of all the risks of waiting to get medical insurance for his or her children.

Like myself, I can’t wait any longer because my husband and my age are catching up. This will cause the insurance charges to increase. Besides, as we age, generally, we also have higher health risks which might impact the premium and benefits offered.

6. Get multiple quotations from different agents

Next, try to gather quotations from a few insurance agents. And for each insurance agent, ask for at least 2 quotations.

Do consider quotations via the online channel (direct through the insurer without going through a third party such as insurance agents).

Although at the time of writing, there are limited medical plans available through the online channel, it is worth taking a look.

And once you’ve seen a few quotations, you’ll be exposed to more options.

7. Choose a good insurance agent

If you’ve decided to get a medical plan through an insurance agent, choose a good insurance agent. Choose someone who is cooperative and helpful.

Because only the insurance agent can get access to their system to generate quotations. Thus, the insurance agent must be willing to follow your request such as applying a minimal Total Sum Assured.

You may ask your friends or family for recommendations. Or, you can fill in the contact form on the insurance provider’s website such as the one provided by Prudential on its PRUMy Child Plus page.

Other things worth taking note

1. Waiting periods

Generally, all insurance and medical insurance plan comes with waiting periods (the number of days before the coverage take effect).

And these are the waiting periods for my son’s policy:

- critical illness (specified illnesses): 60 days

- critical illness (all other covered illnesses): 30 days

- medical benefits (specified covered illnesses): 120 days

- medical benefits (all other covered illnesses): 30 days

- child-specified illness (all covered illnesses): 30 days

- hospitalization due to accidents: Immediately

- accidental benefits: Immediately

I am sharing this so that parents are aware of the waiting periods.

Except for accidents, if anything unfortunate happens during the waiting periods, the policyholder is not covered.

Personally, I only felt relieved when the policy is 120 days old. Because it means we’ve passed the waiting periods. In case of emergencies, we are qualified for the benefits.

2. How do I decide on the premium?

If I followed my actual planning, the premium fits nicely with my budget of RM150 per month.

But because I’ve requested double payor benefits (my husband and me), the finalized premium increased to RM191.00.

To be honest, the premium of RM191.00 per month is quite heavy for us.

Then, I asked myself: Am I willing to spend RM45,840 (RM191 x 12 months x 20 years, assuming my son will be able to continue paying the premium himself at the age of 25 years old) in return for RM1.3 mil yearly limit medical coverage with no lifetime limit?

Thus, thinking about the high cost of medical care and for peace of mind, I decided to proceed with the plan.

The above is how I decided on the premium for the best child medical insurance for my son.

(Note: I am well aware that there are possibilities of an increase in premium in the future due to the rising medical cost. So, the total premium for 20 years could be much higher than RM45,840.)

3. I signed up through a new insurance agent

For my son’s insurance plan, I didn’t sign up through my existing insurance agents. Instead, I signed up through a new insurance agent.

She was an ex-coworker who resigned from her full-time employment to work full-time as an insurance agent.

Although she can’t fully fit all my criteria as a good insurance agent, she was still the one who is willing to tweak the plan based on what I needed.

4. The insurer must be a PIDM insurer member

Since I learned about the many benefits offered by PIDM, I made sure my son’s insurer is a PIDM insurer member.

This is important because just in case something unfortunate happens to the insurer, the eligible benefits will be taken care of by PIDM.

Final thoughts

In summary, the whole process of getting the best child medical insurance for my son was not an easy one.

Fortunately, it’s now already more than two years. This means the waiting period for all of the benefits is over. At least, I am feeling at ease knowing that, just in case there’s an emergency, we have an option other than the government hospital.

If you wish to know which medical plan we signed up for my son, it is PRUMillion Med (Plan 200) that is attached to PRUWith You assurance plan. Personally, the medical plan and policy fit nicely into our requirements.

Have you got yourself or your loved ones protected? How’s the process? Are you happy with the coverage?

I would love to know. Please leave your comment below.

[Disclaimer: I am not a certified financial planner. My sharing is purely based on my own research and personal experience and intended as educational material. In order to make the best financial decision that suits your own needs, you must conduct your own research and seek the advice of a certified financial planner if necessary.]

Image Credits

Featured image by Gerd Altmann from Pixabay

All screenshots were taken by the author

nice post

Hi Lim,

Thank you for your kind words.