For this post, I’ll share my thought on StashAway vs StashAway Simple.

You might have heard of StashAway or StashAway simple but wondering what are their differences. Or maybe you’re currently investing in StashAway but want to know more about StashAway Simple.

Based on my experience investing in both StashAway general investing (we’ll call it StashAway to differentiate it from StashAway Simple) since early 2019 and StashAway Simple since mid of 2021, the two digital wealth management tools do have significant differences.

In this StashAway vs StashAway post, I’ll share the similarities, differences and other things worth knowing about both tools. So that you can have a better idea of both StashAway and StashAway Simple before you decide which one suits you better.

Table of Contents

- Who is StashAway?

- StashAway vs StashAway Simple: 5 similarities

- StashAway vs StashAway Simple: 4 differences

- Other things worth knowing

- StashAway or StashAway Simple is more suitable for you?

- StashAway vs StashAway Simple: Leverage both tools

- Final thoughts

[Disclaimer: I am not a certified financial planner. My sharing is purely based on my own research and personal experience and is intended as educational material. In order to make the best financial decision that suits your own needs, you must conduct your own research and seek the advice of a certified financial planner if necessary.]

Who is StashAway?

StashAway is a digital wealth management platform that offers wealth management solutions for both retail and accredited investors.

As of the end of 2021, StashAway operates in:

- Singapore

- Malaysia

- The Middle East

- North Africa

- Hong Kong

- Thailand

Back in November 2018, StashAway received approval from the Securities Commission Malaysia making it the first robo-advisor for the Malaysian market under the Digital Investment Management (DIM).

Since then, StashAway Malaysia has been offering general investing alternatives through its digital platform in the country. You can read more about my StashAway Malaysia journey in my other post, StashAway Malaysia Review.

In mid of 2020, StashAway launched StashAway Simple, a cash management portfolio for StashAway users to maximize their cash.

To me, StashAway Simple is something like a fixed deposit but without the lock-in periods, minimum deposit and other requirements. You can read more about my experience with StashAway Simple in my other post, StashAway Simple review.

StashAway vs StashAway Simple: 5 similarities

So now that you’ve some ideas about StashAway general investing and StashAway Simple. Let’s look into StashAway vs StashAway Simple.

We’ll start with the similarities between StashAway and StashAway Simple.

From my experience of using both wealth management tools, these are their similarities:

1. Same signing up procedure

Both StashAway and StashAway Simple are from the same fintech platform where everything is completed online.

So, the signing up and onboarding processes are the same such as completing the Know Your Customer (KYC) procedure.

From the screenshot above:

- Invest is referring to StashAway general investing

- Cash Management is referring to StashAway Simple

Both services also have no account set-up or exit fees.

2. Same account management procedure

Since both wealth management tools are on the same platform, the account management procedure is also the same.

Some of the account management procedures are as below:

- depositing funds

- monitoring portfolios performance

- withdrawal of funds

And both wealth management tools offer unlimited and free withdrawals.

3. Both support direct debit

For a smoother and more convenient investment journey, both StashAway and StashAway Simple support direct debit. This is where investors can set up one-time or monthly deposits from their preferred bank to their portfolios.

The objective is to ride on dollar-cost averaging for better returns on investment.

4. No minimum initial investment

Both StasAway wealth management tools also require no minimum initial investment. You can start investing even with RM1.

5. Help to grow your money

And most importantly, both tools are designed to help you to grow your money in their unique ways. Further sharing on their unique ways as below.

StashAway vs StashAway Simple: 4 differences

Based on my experience of using both wealth management tools, below are their significant differences.

1. Different types of investment serving different purposes

One major difference between StashAway and StashAway Simple is they are different types of investments that serve different financial purposes.

StashAway invest in Exchange Traded Funds (ETFs)

For StashAway general investing, your money is invested in a wide range of Exchange Traded Funds (ETFs) according to your selected risk profile, through

Since ETFs are listed and traded on the stock exchanges, generally, StashAway is more suitable for those looking for growth over the medium to long term.

Below is a sample of my StashAway asset allocation.

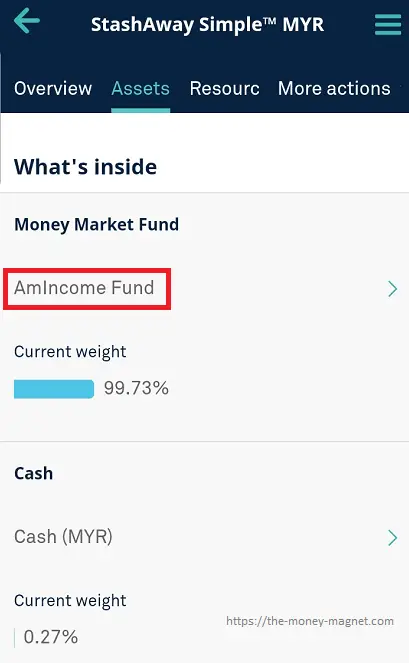

StashAway Simple invest in money market funds

And for StashAway Simple, the underlying fund invests in money market funds and other fixed-income instruments.

Compared to ETFs, generally, a money market fund is more suitable for investors seeking to invest excess cash for the short term with the purpose of potential income. These investors also expect little capital appreciation.

As of the time of writing, my StashAway Simple is invested in AmIncome Fund. Below is a screenshot of my StashAway Simple asset allocation.

For more details about AmIncome Fund, you may refer to AmIncome Fund Monthly Fund Fact Sheet (PDF).

2. Different risk levels

The second difference between the two wealth management tools is on risk level.

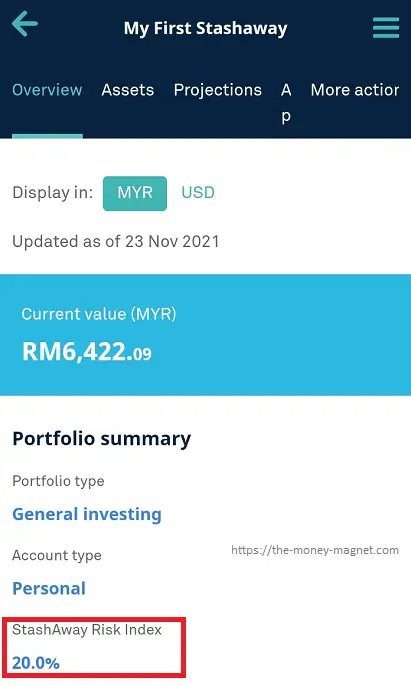

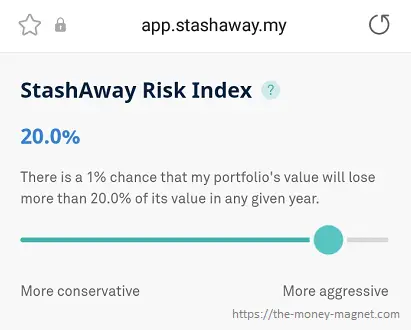

When you invest in StashAway, you can select a StashAway Risk Index (SRI) ranging from 6.5% to 36%. Below is a screenshot of my StashAway portfolio with an SRI of 20.0%.

And the screenshot below explains what it means by StashAway Risk Index 20.0%.

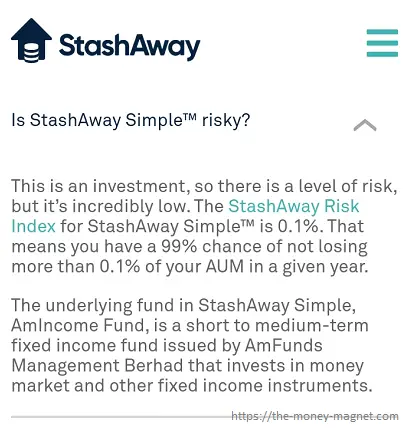

Whereas for StashAway Simple, the SRI is at 0.1%, which according to StashAway is incredibly low-risk. Below is the screenshot from the FAQs on StashAway Simple’s SRI.

StashAway Simple’s SRI of 0.1% means that you have a 99% chance of not losing more than 0.1% of your Asset Under Management (AUM) in a given year.

Based on the SRI, it is clear that StashAway is more suitable for those willing to take on higher risks. On the other hand, StashAway Simple would be a great option for individuals who prefer low-risk and a safer type of investment.

3. Offer different returns on investment

On returns on investment, StashAway offers potentially higher returns compared to StashAway Simple.

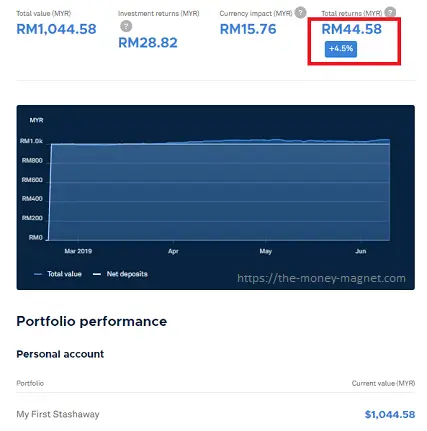

Based on my simple comparison, after about 4 months, my RM1,000 in StashAway generated a total return of RM44.58.

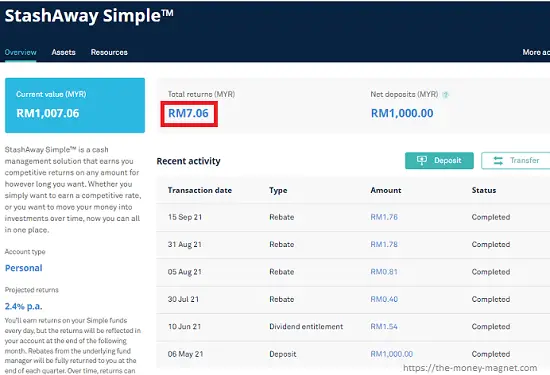

While for the RM1,000 in StashAway Simple, the total return generated is RM7.06 after about 4 months.

It is worth taking note that the 4 months duration are referring to different months and years.

4. Different management fees and other charges

As for fees, StashAway comes with management fees, whereas StashAway Simple does not charge management fees.

Below is a summary of StashAway fees and other charges:

- Management fees range from 0.2% to 0.8% per annum, depending on the total investment amount

- The expense ratio charged by the ETF manager is approximately 0.2% p.a.

- The currency conversion fee charged by the StashAway vendor is 0.1% on the spot rate

And below is a summary of StashAway Simple fees and other charges:

- no management fees

- an approximate 0.5% net expense ratio charged by the underlying fund managers

You can refer to the fee details on the StashAway Malaysia website.

Other things worth knowing

Other than the similarities and differences, here are other things worth knowing for both StashAway and StashAway Simple.

1. You can transfer your fund between the two different portfolios

Something wonderful about the digital platform is that you can easily transfer funds between two different portfolios with just a few clicks.

Say, after trying out StashAway Simple for a few months, you like the platform and wanted to try out StashAway general investing using the same funds.

You can easily transfer the fund from your StashAway Simple to StashAway general investing.

2. You can’t choose the type of fund to invest in

It is worth taking note that, for both tools, you can’t choose the type of fund you want to invest in.

For StashAway, you will need to feel comfortable with the investment decisions by the algorithm based on your preferred SRI. And for StashAway Simple, your money would be invested in a money market fund.

3. Fund withdrawal timeline

Based on StashAway FAQ, below is the fund withdrawal timeline for both tools:

- StashAway withdrawal requires 4 to 5 business days

- StashAway Simple withdrawal requires 3 to 4 business days

I believe it is important to know the withdrawal timeline, especially for StashAway Simple. This is to avoid situations where you urgently need the money but you are not aware that you can’t immediately withdraw your fund from StashAway Simple.

4. Shariah compliance status

As for Shariah’s compliance status, StashAway stated that their portfolios are not strictly Shariah-compliant. And for StashAway Simple, as of the time of writing, the underlying fund is a conventional fund that is not Shariah-compliant.

For those concerned about Shariah compliance, it is best to check the most recent Shariah compliance status of the portfolios and funds from StashAway before starting investing.

StashAway or StashAway Simple is more suitable for you?

Now you might be wondering if StashAway or StashAway Simple is more suitable for you.

Below is my personal opinion for your consideration.

Who is more suitable to invest in StashAway?

StashAway general investing could be a good option in the following situations:

1. You are not planning to use the money within the next few years

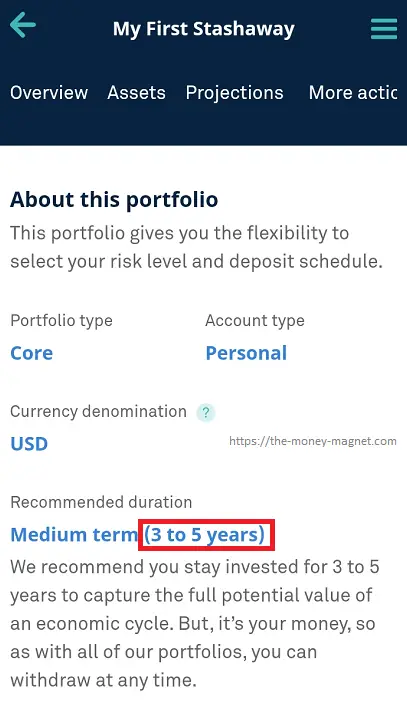

What it means here is that the money is meant for medium to long-term investment. As StashAway invests in ETFs, the recommended investment duration generally is a few years, depending on the SRI.

For example, my StashAway with SRI 20.0% recommends staying invested for the medium-term, that is 3 to 5 years. You may refer to the screenshot below.

So, if you have savings ready for long-term investment, StashAway is a better option compared to StashAway Simple.

2. You are willing to take higher risks with your fund

As mentioned above, StashAway SRI is between 6.5% to 36% compared to 0.1% for StashAway Simple.

If you are willing to take on risks in return for better rewards, StashAway general investing is a better option than StashAway Simple.

3. You want better returns from your investment

From their names, we know that StashAway is for general investing while StashAway Simple is for cash management.

With that said, StashAway has a higher potential to offer better returns compared to StashAway Simple over the medium to long term.

So, if you want better returns and are willing to take on risks, StashAway could be a better option than StashAway Simple.

Who is more suitable to invest in StashAway Simple?

StashAway Simple could be a good option for the situations below.

1. You have excess cash available but you are not ready to put in long-term investment

Among the advantages of StashAway Simple compared to bank fixed deposits is your fund with StashAway Simple is not locked in. This means you can withdraw your fund anytime and still enjoy get to enjoy the projected 2.4% p.a. return.

So, if you have spare cash, you may consider StashAway Simple.

2. You want to make the most from your idle fund while waiting for the right opportunity

If you have some temporary funds waiting for the next opportunity (buying stock, crypto, business purpose), you can take advantage of StashAway Simple to earn the projected 2.4% p.a.

At least you can earn a projected 2.4% p.a. interest. This is much better compared to most savings or current accounts.

3. You prefer to grow your money with lower risk

If you prefer a safer type of financial tool such as a fixed deposit, StashAway Simple with SRI 0.1% is a great alternative. Especially during the time right now, when fixed deposit rates are declining.

Overall, the main benefit of investing in StashAway would be the potential for better returns on investment with manageable risks. While for StashAway Simple, the main benefit would be a great alternative to earn a fixed projected interest of 2.4% p.a. on unutilized cash.

StashAway vs StashAway Simple: Leverage both tools

Since StashAway and StashAway Simple are two wealth management tools with different purposes, you may consider using both tools to:

- maximize the returns from your investment and idle cash

- diversify your investments

Personally, after using the fintech platform, I find it easy to monitor the performance and the returns of both wealth management tools. And most importantly, I am happy with the returns of my portfolios.

Here is a screenshot of both of my portfolios as of November 2021.

Referring to the screenshot above, I started investing in:

- StashAway in early 2019 with RM1,000 followed by another RM4,000 in mid-2019 (total investment of RM5,000)

- StashAway Simple in May 2021 with RM1,000

As for the returns:

- StashAway perform better than most of my unit trust investment (compared with the same investment duration)

- StashAway Simple performs better than my existing fixed deposit placements with an interest rate of 1.7% p.a.

For the latest updates on both portfolio performance, you may refer to my StashAway Malaysia Review and StashAway Simple Review.

Final thoughts

With the above sharing on StashAway vs StashAway Simple, I hope you have a better picture of the two wealth management tools.

In my opinion, both StashAway and StashAway Simple are wealth management solutions to grow your money. The best part is that you can leverage both tools so that you can reap every opportunity to grow your money, be it the fund is temporarily unused cash or savings meant for long-term investment.

In the end, you’ll still need to try out the fintech platform yourself to see if they are the right financial tool for you. For that, take advantage of the discounted fees when you sign up using my StashAway promo code. The promo link comes with 50% fees for the first RM100,000 invested for 6 months.

Just remember to make a deposit (any amount) within 30 days of signing up to entitle you to the discounted fees. You’ll find more details of the promotion under the StashAway promo code in my StashAway Malaysia Review.

Lastly, you may want to check out my sharing on another Robo-advisor platform, Kenanga Digital Investing (KDI) Review. Don’t forget to redeem the RM10 KDI Invest sign-up bonus.

Image Credits

Featured Image by Orlandow from Pixabay

All screenshots were taken by the author