Should you transfer your fixed deposit to EPF (Employee Provident Fund) or KWSP (Kumpulan Wang Simpanan Pekerja)?

In this post, I am going to share my thought about moving your savings from fixed deposit to EPF savings.

Table of Contents

- Why transfer your fixed deposit to EPF?

- The pros of transferring your fixed deposit to EPF savings

- Cons of transferring your fixed deposit to EPF savings

- Should you transfer your fixed deposit to EPF savings?

- Other alternatives to fixed deposit

- Final thoughts

[Disclaimer: I am not a certified financial planner. My sharing is purely based on my own research and personal experience. To make the best financial decision that suits your own needs, you must conduct your own research and seek the advice of a certified financial planner if necessary]

Why transfer your fixed deposit to EPF?

Before the pandemic, the average fixed deposit (FD) interest rate for banks in Malaysia is around 3% per annum. During the pandemic, the fixed deposit interest rate dropped to around 2% per annum. This is due to Bank Negara Malaysia’s (BNM) decision to cut the overnight policy rate (OPR) to help the economy to recover.

If you have a fixed deposit at the bank, it is understandable that you will start looking around and considering better alternatives to grow your hard-earned money.

So, when EPF announced its 2022 dividends of 5.35% for Simpanan Konvensional and 4.75% for Simpanan Shariah, you started to do some simple calculations:

- RM10,000 in fixed deposit: yearly interest is RM200 (RM10,000 x 2%)

- RM10,000 in EPF savings: yearly dividend is RM535 (RM10,000 x 5.35%)

There’s a difference of RM335. Then you increase the saving amount to RM60,000*.

- RM60,000 in fixed deposit: yearly interest is RM1,200 (RM60,000 x 2%)

- RM60,000 in EPF savings: yearly dividend is RM3,210 (RM60,000 x 5.35%)

Whoa! There is a significant difference of RM2,010!

That imagery of better return makes you start thinking about transferring your fixed deposit to your EPF account.

But, hold on. Is there any other thing to consider besides the assumption of a better return? Let’s take a look at the potential pros and cons of moving your fixed deposit to your EPF savings.

(*RM60,000 because EPF only allows a maximum of RM60,000 yearly for EPF Voluntary Contribution schemes such as Self Contribution, i-Saraan, and other voluntary schemes.)

The pros of transferring your fixed deposit to EPF savings

These are the potential benefits of transferring your fixed deposit to EPF savings:

1. Possibility of higher returns

Comparing the current fixed deposit interest rate of about 2% with the 2022 EPF dividend rate of 5.35% for Simpanan Konvensional, there is a significant difference of about 3.35%.

With the average EPF dividend rate for the past 10 years at 6%, no wonder you are thinking to transfer your fixed deposit to EPF savings.

There are possibilities that you’ll earn higher returns from EPF savings.

But, do take note that past performance is not necessarily indicative of future results.

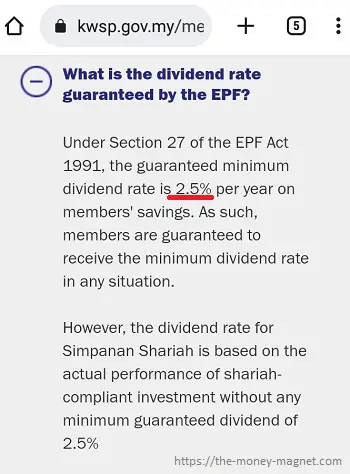

2. EPF guaranteed dividend rate

For Simpanan Konvensional, EPF’s guaranteed dividend rate is 2.5% per year on members’ savings. Although considered low, 2.5% is still slightly higher than the average 2% interest rate offered by most local financial institutions at the current time.

Thus, if your EPF account is under Simpanan Konvensional, at least you’ll receive a minimum of 2.5% yearly dividend rate.

3. A great way to grow your EPF savings

Do you agree if I said any additional contribution made to your EPF account shall upsize your EPF savings?

That’s because you can’t withdraw the fund until you reach the official EPF retirement age, which is 55 years old. Although you may request for early partial withdrawal subject to EPF withdrawal terms.

So, transferring any amount from your fixed deposit to EPF savings shall boost your retirement savings.

4. Might be eligible for government incentive

Have you heard of i-Saraan? It is one of the voluntary contribution schemes offered by EPF, targeting those who are self-employed.

If you are an EPF member below 60 years old and had registered for the i-Saraan scheme, you are eligible for the matching 15% government incentive with a maximum of RM300 per year for the year 2023.

So, if you are transferring RM2,000 from your fixed deposit to EPF through the i-Saraan scheme for the year 2023, you are eligible for the RM300 incentive.

For your information, I am currently contributing to i-Saraan. You can read about the scheme in my EPF i-Saraan blog post.

5. Enjoy savings from income tax relief

Your fixed deposit is not eligible for income tax relief. But, your EPF contribution is eligible for income tax relief. As for the assessment year 2022, LHDN personal tax relief for EPF contribution is up to RM4,000.

This means EPF members who have not maximized their income tax relief may enjoy tax savings when they shift some of their fixed deposits to their EPF accounts.

While self-employed may choose to contribute through i-Saraan, EPF members under full-time employment may choose to make their own voluntary contribution through the EPF Self Contribution scheme.

Cons of transferring your fixed deposit to EPF savings

Below are two disadvantages of transferring your fixed deposit to EPF savings:

1. Your savings are locked-in

In my opinion, the major drawback of transferring from a fixed deposit to the EPF saving would be the fund is locked in. In other words, you don’t have the flexibility to withdraw your savings, unless you:

- reach the official EPF retirement age which is 55 years old;

- reach 60 years old for contributions made between 55 to 60 years old (Akaun Emas);

- you meet the full or partial withdrawal rules mentioned on the EPF website.

On the other hand, you can request to uplift or withdraw your savings in a fixed deposit anytime you wish. Even though premature withdrawal may result in no or partial interest paid, you still get full access to your savings.

2. Limited control over investment options

Another disadvantage of transferring your fixed deposit to EPF is you have limited control over how to invest your EPF fund.

Although you are allowed to withdraw a certain percentage of the savings in your EPF Account 1 under Member’s Investment Scheme, you don’t have the full flexibility as compared to withdrawing your fixed deposit for other types of investments.

I believe flexibility is an important factor in managing our personal finance. Because over the long run, you might want to consider the following:

- As the pandemic recover, what if the fixed deposit rate increase to a better rate than EPF’s guaranteed minimum 2.5% dividend rate?

- How about investing the money in future technology that has the potential to offer more attractive returns such as cryptocurrency and blockchain technology?

Therefore, the above are the possible downsides when you transfer your saving from a fixed deposit to EPF savings.

Should you transfer your fixed deposit to EPF savings?

So now, after knowing the potential pros and cons, do you still want to transfer your fixed deposit to EPF?

In my opinion, I would say it depends on your situation and personal preferences. For that, you may find some of the questions below worth considering asking yourself before deciding whether to transfer your fixed deposit to EPF:

- Are you ok if you are only able to withdraw the fund after x years (x years is the years until you reach 55 years old or 60 years old)?

- Do you need to boost your EPF savings?

- Have you maximized your EPF tax relief?

- Are you eligible for EPF i-Saraan?

- What are some of the potential investment opportunities you might lose?

- Do you have sufficient emergency savings?

- Do you need the savings in your fixed deposit before you reach 55 or 60 years old?

- Will you regret your decision if the fixed deposit rate increase to a rate much higher than EPF dividend rates?

As for me, I have not transferred my fixed deposit to EPF.

I feel comfortable having a portion of my savings under a fixed deposit. Although I have plans to transfer a portion of my fixed deposit to other alternative investments such as cryptocurrency, Robo-advisory platforms, and crowdfunding.

The main reason is I want to have the control and freedom to invest and grow my savings on my own terms and conditions.

And for my EPF, since I left my full-time employment in 2018, I do contribute to i-Saraan. But the fund is from my savings and not from my fixed deposits.

Other alternatives to fixed deposit

If you are looking for alternatives for better returns on your savings, you might find the following useful:

- Look around for better deals on fixed deposits such as those offered by the financial comparison website RinggitPlus.

- Try out a Robo-advisory platform:

- StashAway Malaysia general investing offers lower fees compared to unit trust.

- StashAway Simple offers flexible and no-fee cash management solutions.

- Kenanga Digital Investing (KDI Invest and KDI Save) offer affordable investing opportunities.

Before deciding on any new investment, do take time to understand the terms and conditions including the risks involved.

Final thoughts

With the above, I hope you can have a better idea of the potential benefits and drawbacks of transferring your fixed deposit to EPF.

Whatever your decision, the most important part is you must know what you are doing. Don’t mislead by others’ personal finance decisions as every one of us is different. Make your own decision based on your own unique needs and preferences.

If I have missed out on any important points, please comment below.

Lastly, if you enjoy this blog post, you might find my other sharing on EPF and retirement planning useful as well.

Image Credits

Featured image by Mohamed Hassan from Pixabay

Thanks for gathering the information and making it easy to digest.

Hi Shel,

Thank you for your kind words. It means a lot to me 🙂 And glad that that you find the blog post easy to digest. Have a great day!