This post is about EPF Self Contribution.

Most of us are aware of EPF (Employees’ Provident Fund) or KWSP (Kumpulan Wang Simpanan Pekerja). Because employers and employees in Malaysia must contribute a portion of their monthly salary to EPF savings as a retirement fund.

As for the Self Contribution or KWSP Caruman Sendiri, I believe many of us are still unaware of it.

In this post, I’ll share all I know about EPF Self Contribution.

Since this is a long post, feel free to jump to whichever section applies to you.

Table of Contents

- What is EPF Self Contribution?

- Who can contribute to EPF Self Contribution?

- What are the minimum and maximum contribution amounts?

- EPF Self Contribution vs i-Saraan

- 4 EPF Self Contribution benefits

- EPF Self Contribution age limit

- How to make payment for EPF Self Contribution?

- How to pay EPF Self Contribution online?

- EPF Self Contribution FAQs

- 1. Do I need to register as an EPF member before contributing to EPF Self Contribution?

- 2. How long does it take before the contribution is reflected on the EPF statement?

- 3. Can you contribute RM60,000 in one lump sum?

- 4. Do you need to contribute monthly?

- 5. When is the best time to make the EPF contribution?

- 6. What is the dividend rate for EPF Self Contribution?

- 7. The Self Contribution is updated to which EPF account?

- 8. Can I make withdrawals from my EPF Self Contribution?

- 9. Does EPF withdrawal subject to tax deduction?

- Final thoughts

What is EPF Self Contribution?

Based on the EPF Act 1991, employers and employees are required to contribute to EPF. Hence, all employers and employees must contribute according to the rules and regulations of EPF.

Aside from this mandatory contribution, EPF members may choose to make a voluntary contribution.

Through voluntary contribution, EPF members can contribute to their EPF account anytime with any amount, as long as the amount does not exceed the allowed maximum contribution (further explanation below).

EPF offered different types of voluntary contributions. Among those are the three voluntary contributions stated below, including the Self Contribution scheme.

1. EPF Self Contribution

One of the EPF voluntary schemes is the Self Contribution scheme. Here is some brief description of the scheme:

- EPF Self Contribution is an EPF scheme where registered EPF members may make additional contributions to their EPF savings with any amount and at any time.

- This includes salaried employees, self-employed, freelance workers, and anyone who wishes to better prepare for their retirement.

2. EPF i-Saraan

Another well-known EPF voluntary scheme is the i-Saraan. Here is some brief description of i-Saraan:

- i-Saraan is a voluntary retirement scheme targeting self-employed Malaysians and those who do receive monthly wages.

- i-Saraan comes with government incentives to encourage its members to continue saving for retirement. You can read more about the scheme in my other on i-Saraan.

3. EPF Top-Up Savings Contribution

Another EPF voluntary scheme is the Top-Up Savings contributions:

- The EPF Top-up Savings Contribution is a scheme where EPF members can top up EPF savings for their parents, spouse, or children.

For all of the above four schemes, Malaysian citizens who are registered EPF members are welcomed and encouraged to contribute voluntarily to their EPF savings, according to the type of contribution.

The main objective is to encourage Malaysians to save for retirement.

With that said, EPF Self Contribution is one of the EPF voluntary contributions where its members can make additional contributions whenever they can with any amount they feel comfortable with.

This is also where self-employed and those without employers can start contributing to EPF.

Who can contribute to EPF Self Contribution?

According to the EPF website, these are the requirements for Self Contribution:

- Malaysian citizen and Permanent Resident

- Registered EPF member

In other words, Malaysians who are registered as EPF members are allowed to make contributions to the retirement scheme.

Some examples of those eligible to contribute are as below:

- Self-employed individuals

- Owners of a sole proprietorship or business partners who do not receive wages

- Existing EPF member who is under full-time employment

Example of those who can contribute to EPF Self Contribution

Below, I share more examples of those who can contribute to the Self Contribution scheme:

- Farmers, fishermen, hawkers, and Grab drivers;

- Business owners;

- Commission-based agents;

- Freelancers;

- Professionals;

- Housewives;

- Pensionable employees;

- Malaysian working overseas;

- Salaried employees.

For those, not salaried employees such as self-employed individuals, I would suggest registering and contributing through EPF i-Saraan.

That is because i-Saraan comes with a 15% matching government incentive (maximum RM500 in a year, for year 2024).

Further below, I’ll share the difference between the Self Contribution scheme and i-Saraan.

Can a self-employed person contribute to EPF?

Yes, as mentioned above, self-employed individuals are encouraged to contribute to EPF either through Self Contribution or i-Saraan.

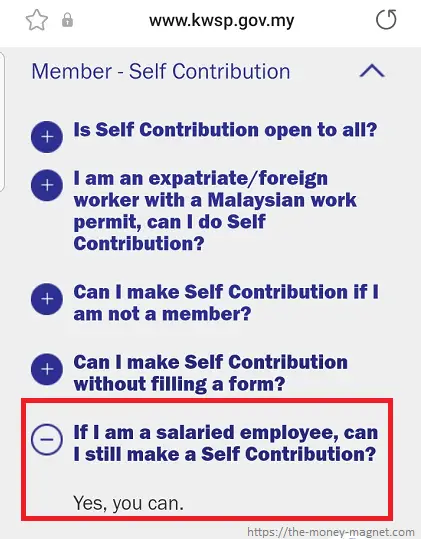

Can a salaried employee contribute to EPF Self Contribution?

Yes, a salaried employee can make additional EPF contributions through the Self Contribution scheme.

It is stated clearly on the EPF website’s FAQs that a salaried employee can still self-contribute to EPF.

You may refer to the FAQ screenshot below.

So, employees who wish to contribute more than the mandatory EPF contribution may do so by contributing through the scheme.

Can Malaysians working overseas contribute to EPF Self Contribution?

Yes, Malaysians working overseas can contribute to EPF through the scheme. But, first of all, they must register themselves as an EPF member.

Then, they can either contribute through the EPF Self Contribution or i-Saraan.

Similar to those self-employed, I would highly recommend that Malaysians who work overseas register and contribute through i-Saraan. Through i-Saraan, you can take advantage of the government incentive.

I find the article from The Star Online on ‘EPF contributions for Malaysian working abroad‘ very helpful.

Can government servants contribute to EPF savings?

Yes, government servants can contribute to EPF savings through the EPF Self Contribution scheme. Further reading is available on The Star Online’s ‘Civil servants can contribute to EPF‘.

Just make sure to register as an EPF member before making the voluntary contribution.

What are the minimum and maximum contribution amounts?

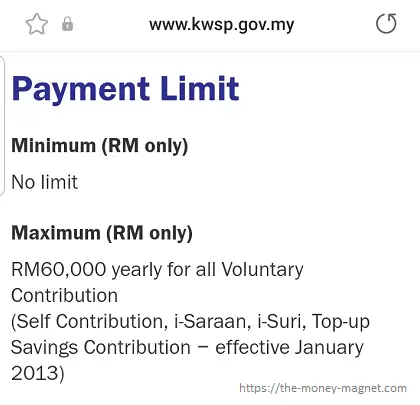

According to the EPF website, there is no minimum contribution amount for the EPF Self Contribution scheme (except for the RM10.00 minimum for contributions through the i-Akaun mobile app).

You may refer to the screenshot below from the EPF website.

As for the maximum contribution amount, effective from 2013, the payment for EPF Voluntary Contribution including EPF Self Contribution is capped at RM60,000 per year.

Are you currently employed and wondering if the contribution limit of RM60,000 a year including the EPF contributions is deducted from your salary?

The answer is ‘No‘. The RM60,000 limit in a year is solely for the contribution made through EPF Self Contribution and other voluntary contributions. It does not include EPF contributions deducted from your monthly wages.

EPF Self Contribution vs i-Saraan

In early 2019, I registered myself for EPF i-Saraan (previously known as 1Malaysia Retirement Savings Scheme or SP1M).

From my understanding, here is the differences between the EPF Self Contribution and i-Saraan scheme:

1. Government contribution of 15%

For the Self Contribution scheme, there’s no government contribution.

On the other hand, for i-Saraan, the member shall receive a 15% contribution from the government on the amount contributed, subject to a maximum of RM500 a year for the year 2024.

However, the government contribution is limited to i-Saraan members who are under the age of 60.

2. Eligibility

As for eligibility, all Malaysians who are registered EPF members can contribute to EPF Self Contribution.

Whereas, salaried employees or those under employment who received regular incomes are not eligible to participate in i-Saraan.

So, i-Saraan is only for those who are not in any employment.

3. Registration needed for i-Saraan

For the Self Contribution scheme, there’s no additional step needed apart from being an EPF member. In other words, you do not need to fill in an additional EPF form before contributing.

But for i-Saraan, due to government contribution and the eligibility mentioned above, the interested EPF member needs to register for i-Saraan by visiting the nearest EPF kiosks, or counter or registering online.

For this, you can read my sharing on i-Saraan registration.

4 EPF Self Contribution benefits

Whether you are in full-time employment, self-employed, or retiree, you can reap the benefits of contributing through Self Contribution.

Here are some of the benefits:

1. Preparing for a bigger retirement fund

For the self-employed who choose to contribute through EPF self Contribution instead of i-Saraan, contributing to the scheme is a great way to force yourself to prepare for your retirement.

As you can contribute any amount anytime you feel comfortable, with proper discipline, your retirement savings shall grow over the years.

For the salaried employee, with the EPF contribution rate of between 7% to 11% (employee) and 12% or 13% (employer), most likely your EPF savings are not sufficient to support your retirement years.

Especially if we wish to continue to live with the current lifestyle.

Thus, contributing to the scheme will help you to prepare a bigger fund for your retirement.

2. Reaping the advantage from high EPF dividends

The average EPF dividends rate for the past 10 years is 6.035% with the lowest rate being 5.20% (year 2020) and the highest rate being 6.9% (year 2017).

So, when EPF members make a contribution or an additional contribution through the scheme, they gain an advantage from the high EPF dividends.

3. To fully utilize your income tax relief

Another benefit of this scheme is income tax relief.

For the 2022 assessment, Malaysia IRB (Inland Revenue Board) is giving income tax relief of RM4,000 for contributions to EPF and other approved schemes.

Self-employed may want to take advantage of the EPF tax relief. And an employee who has not reached the maximum of RM4,000 may also consider topping up their EPF through this scheme.

4. Opportunity to participate in EPF initiatives

As an EPF members (especially self-employed individuals), you may get the opportunity to participate in great EPF initiatives such as:

- i-Lindung

- Participating in i-Lindung gives you an opportunity to enjoy better insurance coverage for you and your loved ones.

- i-Invest

- Participating in i-Invest to enjoy lower initial sales charges for selected unit trust investment.

All the above benefits shall grow your EPF savings so that you can better prepare yourself for a more comfortable retirement.

EPF Self Contribution age limit

Some of my readers asked about the age limit of EPF contributions, such as:

- Can a retiree contribute to EPF Self Contribution?

- What is the age limit to contribute to EPF Self Contribution?

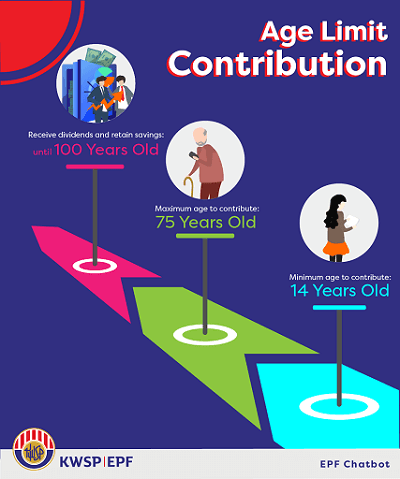

According to EPF, members can continue to contribute until the age of 75 years. And members will obtain dividends as long as there are savings in the EPF account until the age of 100 years.

Here is a helpful infographic on the EPF contribution age limit from EPF Chatbot, Elya.

From the infographic above, it states clearly that:

- The Minimum age to contribute to EPF is 14 years old;

- The Maximum age to contribute to EPF is 75 years old;

- EPF members may receive dividends and retain savings until 100 years old.

Thus, EPF members including retirees may continue to contribute until the age of 75 years old.

Do take note that, any contributions to EPF after age 55 will be parked under a separate account, Akaun Emas. And members can only withdraw the accumulated contributions in Akaun Emas at age 60.

If you want to know more details, you may visit Akaun Emas on the EPF website.

How to make payment for EPF Self Contribution?

You can contribute to EPF Self Contribution scheme through the following channels:

1. Mobile app i-Akaun

If you are using the i-Akaun mobile app, you can easily make your EPF Self Contribution through the app.

Just take note, the minimum payment required through i-Akaun mobile app is RM10.00.

You can refer to the FAQs and step-by-step on the EPF website.

2. Online banking

Secondly, you can make the Self Contribution payment through online banking.

In my personal opinion, I find that online banking is the easiest, fastest, and simplest method to make EPF payments.

Because members can do it in their comfort at any time of the day. Furthermore, contributions made through online banking do not require form submission.

Currently, this is the list of banks where EPF members can contribute to online transfers:

- MBSB Bank

- Maybank

- Public Bank

- CIMB Bank

- Kuwait Finance House

- RHB Bank

- Bank Muamalat

- Bank Islam

- Alliance Bank

- Hong Leong Bank

For the most recent and updated list of participating banks, always refer to the official EPF website.

3. Through bank agent counters

Thirdly, you may make your EPF Self Contribution payment through bank agent counters.

As of the time of writing, the participating bank agent counters are:

- Maybank

- Public Bank

- RHB Bank Berhad

- Bank Simpanan National (BSN)

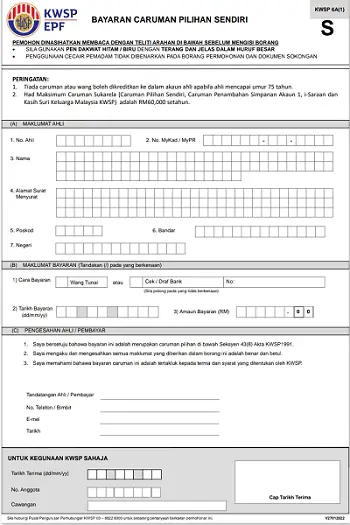

Do take note that for contribution through the bank agent counter, you will need to fill in Form KWSP 6A(1) as well.

4. Through a registered bank agent

Besides through selected bank agent counters, EPF members can also make payments for Self Contribution through Bank Agent (EB) BSN.

To be on the safe side, do remember to write your NRIC and EPF number on the reverse side of the cheque.

5. EPF counters nationwide

Lastly, you may contribute to the Self Contribution scheme by making cash payments (maximum RM500) or cheque payments at EPF counters nationwide.

And do take note that you will need to fill in Form KWSP 6A(1) (PDF).

You’ll find the sample form KWSP 6A(1) below.

As the payment channels may change from time to time, for the most recent updates, always refer to the official EPF website.

How to pay EPF Self Contribution online?

Personally, I successfully made my i-Saraan contribution through online transfer. You can find my sharing in the blog post below:

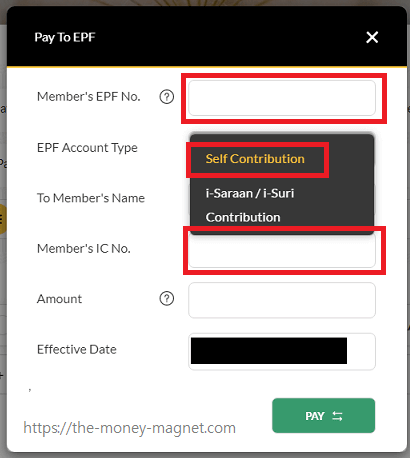

From my experience, I found out the contribution method for EPF Self Contribution is similar to i-Saraan. The difference is choosing the correct EPF Account Type when making the online contribution.

Because if you choose the wrong account type, you might need to walk in or write to the EPF for correction.

So, for EPF Self Contribution, make sure you choose ‘Self Contribution’ or ‘Bayaran Caruman Pilihan Sendiri’ to avoid any issues with your EPF payment.

You’ll find further details below.

How to pay EPF Self Contribution through Maybank online (Maybank2U)?

When making a payment through Maybank2U, make sure to select ‘Self Contribution‘ under EPF Account Type as shown in the screenshot above.

Do take note to enter your EPF number and NRIC as well.

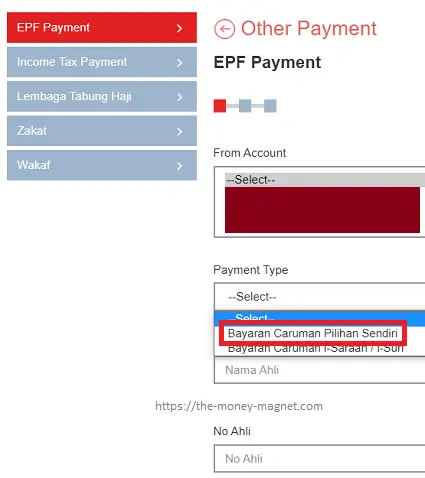

How to pay EPF Self Contribution through Public Bank online?

As for Public Bank online, the step-by-step on how to make payment for EPF Self Contribution is also similar to my sharing on how to make EPF i-Saraan Contribution through Public Bank online.

The only difference is you’ll need to choose ‘Bayaran Caruman Pilihan Sendiri‘, as shown in the screenshot above.

And do take note to enter your EPF account number and NRIC number correctly.

Personal tips on paying EPF Self Contribution online

If you are making an online payment to EPF for the first time, I can understand if you are worried about the transaction.

The tips below might be helpful:

- Try out with a small contribution amount, say RM10.

- Make sure you entered the correct EPF account number and NRIC.

- See if the transaction is successful and the amount appears in your EPF statement within 3 working days (if you are not using EPF i-Akaun, it is advisable to register for it. EPF i-Akaun makes managing the EPF account a lot easier).

- If the amount appears in your EPF statement, you may start transferring your actual contribution amount.

With the above, you’ll have real experience and more confidence when you make subsequent EPF payments online.

EPF Self Contribution FAQs

Since I published this post, I’ve received a number of inquiries related to the scheme from my blog readers.

You may refer to some of the frequently asked questions (FAQs) below. Please take note that these answers are based on my own experience.

If you have inquiries related to EPF contributions, it is best to contact EPF officially.

1. Do I need to register as an EPF member before contributing to EPF Self Contribution?

Yes, you must register as an EPF member before you can start contributing through EPF Self Contribution.

If you are already an EPF member, you don’t have to register again for the scheme.

In other words, as long as you have your EPF number, you can start making contributions to the scheme.

Unsure whether you have an EPF number? You can read my other post on how to check EPF number (through calls, EPF live chat, kiosks, EPF online inquiry, and other options).

If you are not an EPF member yet, you can easily register for an EPF account through EPF Self-Service Terminal (kiosks) or at any EPF counter nationwide. Just bring along your MyKad for verification purposes.

2. How long does it take before the contribution is reflected on the EPF statement?

For electronic transfer, it takes up to 3 working days before the contribution amount is reflected on the EPF statement.

For non-electronic transfers, it takes up to 14 working days before you can view the amount on your EPF statement.

Personally, I’ve been using online transfer for all my voluntary EPF contributions. All my contributions were updated within 1 to 3 working days.

3. Can you contribute RM60,000 in one lump sum?

In 2022, one of my family members successfully made a lump sum contribution of RM60,000 to his EPF Self Contribution.

He made the contribution through the bank counter (Public Bank) together with a completed KWSP form 6A(1).

Do remember to make a copy of the completed KWSP form 6A(1) for your record.

4. Do you need to contribute monthly?

EPF Self Contribution is a voluntary contribution scheme.

So, you are not required to contribute monthly. You may contribute your own schedule with the amount you feel comfortable with.

5. When is the best time to make the EPF contribution?

There’s a difference between contributing RM60,000 at the beginning of the year or the end of the year. Because the EPF dividend calculation is based on “Modified Aggregate Daily Balance”.

EPF website on Dividend calculation FAQ mentions that contributions for a particular month will be eligible for dividends based on the last day of the contribution month until the last day of the year.

Do also take a look at the EPF dividend calculation sample under ‘How is the annual dividend calculated?’. It’s very helpful.

So, the earlier you make the contribution, the more dividend you’ll receive.

6. What is the dividend rate for EPF Self Contribution?

The dividend rate for EPF Self Contribution is the same as the yearly EPF dividend rate announced by EPF.

7. The Self Contribution is updated to which EPF account?

From my own contribution, I can see that 70% is channeled to EPF Account 1. And the remaining 30% is channeled to EPF Account 2.

8. Can I make withdrawals from my EPF Self Contribution?

Withdrawal from EPF Self Contribution is following the same procedure as the normal EPF withdrawal.

For example, you may make a withdrawal from your EPF Account 2 to pay your housing loan, subject to EPF’s other withdrawal requirements.

9. Does EPF withdrawal subject to tax deduction?

EPF withdrawals are exempted from income tax.

You may refer to the clarification on EPF website: Home>Member>Overview, under ‘Your Entitlement’ tab, look for ‘Your Benefits’ under ‘Tax Exemption’

Final thoughts

With the above sharing, I hope you are aware that you can utilize EPF Self Contribution to grow your EPF savings.

Or at least, now you are aware that self-employed individuals and those without an employer can still contribute to EPF through the scheme. While employees may contribute through Self Contribution if they wish to make additional contributions on top of the statutory deductions from their monthly salary.

If you have friends or relatives who are not aware about the self-contribution scheme, do them a favor by sharing this write-up with them.

Any other things you wish to know about the EPF Self Contribution scheme? Please leave your comment below.

Let’s save more and hopefully secure bigger EPF savings for our retirement years.

Lastly, feel free to read my other post on EPF and retirement planning.

Disclaimer: This blog post is based on my experience and research as an EPF member. I tried my best to keep this blog post updated. If you’ve found any of the information above outdated or incorrect, please leave a comment below or send me an email. For the most recent updates, please refer to the official details published on the EPF website.

Image Credits

Screenshots are taken by the author

I was under employment previously but now under freelance work. Do I need to open new EPF account for personal contribution? Would the EPF account number same as the existing EPF account that I am holding (with employer) previously?

Do I need to register a new EPF account? Please advise.

Hi Frank, there is no need to register for a new EPF number. For the normal epf self contribution, you can just contribute to your EPF account through online banking via selected banks.

Since you are freelancing now, you might want to consider EPF i-Saraan. For EPF i-saraan (for self-employed, freelance..), you need to go to EPF office to ‘activate’ this scheme for the 15% matching contribution from the government. EPF i-saraan also using the same EPF number.

Anyway, you can call EPF centre to ask if there’s other ways to ‘activate’ i-saraan.

Do read my other sharing on EPF i-Saraan including how to transfer the money through online banking to EPF i-saraan contribution.

Hope this helps.

Hi, Michelle.

Thank you for your advise. I quit my previous job end of last year.

As the employment market is quite bad for now, I am working on freelance basis. I might go back to full time employment once the situation improves. The reason for me to inquire on EPF self contribution as it could help to save some taxes to be incurred for this year.

Do I need to inform EPF that I am not longer under employment before proceeding for EPF self contribution?

In consideration of my current situation, what is your advise? Should I just go for self contribution as I might go back to full time employment? Or go for i-Saraan?

Appreciate your advise.

Hi Frank, for EPF self contribution, there’s no need to inform EPF. Even if you’re back to full-time employment with EPF contribution (from you and your future employer), you can still make additional EPF contribution through self contribution.

But for i-Saraan, you need to inform EPF that you wish to apply for i-Saraan so that you’re entitled to the 15% matching incentive from our government (maximum RM250/year incentive from our government until the year 2022).

Both self contribution and i-Saraan contribution are eligible for tax relief.

Hope the above helps.

Hi Michelle,

Thanks for your advise. Is there a need to inform EPF that I am no longer under employment before proceeding for EPF self contribution?

Current employment market is bad, thus I am working on freelance for now. I might return to full time employment once the market condition improves.

Noted the advantage of the EPF i-Saraan. In view that I still need to report my income for income tax purpose. Should I just proceed for self contribution for now?

Appreciate your view on this.

Hai,Michelle,

i am EPF Member and self- employed .i am about starting to do the EPF self-contribute via Maybank2u. Just want to know that the payment i make to EPF self-contribute will it be appeal monthly in the log-in KWSP system ? or how can i check my monthly self-contribution?

please give advise. & Thanks in-advance !

Ms Lim ( KL)

Hi Ms Lim,

All EPF contributions will appear on EPF or KWSP system, including EPF self-contribution. In the EPF statement, you’ll see the ‘transaksi’ where it shows the type of contribution.

You can refer to the screenshot from my EPF i-Akaun on updates of the EPF contribution.

By the way, since you’re self-employed, you may consider registering for EPF i-Saraan. Because there’s a matching incentive of 15% (up to RM250 per year) for EPF i-Saraan contribution, from the year 2018 until the year 2022.

Hope the above helps.

Thank you so much! you are so helpful!

Thank you for your kind words, Ms Lim 🙂

HI Michelle,

I m salaried employee, but would like to top up self-contribution for future retirement. As stated that the limit is RM60,000 per annum. May I know is that the combined limit for salaried & self contribution or solely for self contribution.

Your advice is much appreciated. Thanks.

Regards,

Steven Chong

Hi Steven,

Thank you for your comment.

From EPF website, it mentions that with effect from January 2013, the contribution limit of RM60,000 per year is for all Voluntary Contribution (Self Contribution, i-Saraan, i-Suri and Top-up Savings Contributions). So, the RM60,000 should be solely for Self Contribution.

Btw, I had sent an enquiry to the EPF team for clarification. Once I received the reply, I shall update you and on my blog too.

Hi Again Steven,

I received confirmation from the EPF team that the RM60,000 for the voluntary contribution is solely for voluntary contribution including self-contribution. Which means the RM60,000 excludes the EPF contribution from your wages. Hope this helps.

Thanks for advice and confirmation. Really appreciate that. Thanks again.

Hi Steven, my pleasure. Thank you for the question. I am sure there are others wanting to know whether the RM60,000 for voluntary contribution is inclusive or exclusive of wages. I’ve updated this detail in my sharing.

HI Michelle,

I’m currently employed in a bank and every month mandatory contribution has been made to EPF by me and the bank. Let say if I got extra fund , let say RM1000 , I still can contribute to EPF at any time subject to RM60k per year right? And if I use online transfer will be easier because no need to fill up any form right?

I have been contacting KWSP but so far didn’t get any answer.

Hi Tham, thank you for your comment. Yes, on top of the monthly EPF contribution deducted from your salary, you still can make voluntary contribution, maximum RM60,000 in a year.

Yes, online banking is much easier and no form needed. Just remember to choose ‘EPF Self Contribution’ and enter your EPF number correctly. If you are worried, perhaps try with a small amount. Once the transaction appear in your EPF statement, you can make additional contribution.

So far, EPF team replied all my enquiries. Perhaps need to wait a few working days.

Hope the above helps.

Thanks Michelle! This article is very useful!

Hi Tham, thank you for your kind words 🙂 Perhaps leave a comment here once you’ve successfully made your contribution through EPF Self Contribution. I think that will helps others looking for similar information.

Hi Michelle,

I was previously employed but currently, self-employed. My question is if I apply and contribute to I-Saraan to utilize the government incentive and later decided to go back to full-time employment, what will happen to this account? And will there be any problems for future employment contributions? Please advise, thanks.

Hi Ella, thank you for your comment.

FYI, our EPF number remains the same even for i-Saraan.

I’ve asked the same question on the impact of our EPF contribution if I am back to full-time employment when I registered for my i-Saraan in January 2019.

The officer told me, they’ll detect when receiving the EPF statutory contribution from the employer under statutory contribution and thus no longer on i-Saraan contribution.

I suggest you clarify with the EPF team when you’re applying for i-Saraan.

Hope the above helps.

Thanks for the clarification Michelle, will check with EPF directly. Cheers 🙂

My pleasure, Ella 🙂

HOW IF I accidentally voluntary contribution, MORE 60,000 eg ON the YEAR 2020 we put more extra 20,000 – more maximum RM60,000 in a year.

What will happen? ARE THE MONEY WILL RETURN BACK TO US OR

KWSP WILL HOLD OUR MONEY. WAIT UNTIL the NEXT YEAR 2021. KWSP WILL CREDIT TO OUS KWSP ACCOUNT?

Hi Looi,

Thank you for your comment.

But, sorry I am not able to assist on your questions about EPF voluntary contribution more than RM60,000 in a year.

I suggest you contact the KWSP team through KWSP website.

You can either send them an enquiry or call them at their call centre. So far, the EPF team replied all my enquiries, although some times it might take a few working days.

Hope this helps.

They will return the money via the same bank you transferred. I’ve asked before.

Hi Allen,

Thank you for sharing. Do EPF members need to send a request to return the excess contribution?

Hi Michelle,

Would like to confirm, do I need to fill in any form to register for the self-contribution before I pay directly via online banking? If yes, do I need to visit the branch to submit the form?

Hi Chloe,

Thank you for your comment.

For EPF Self Contribution, if you are an existing EPF member, there’s no additional registration needed for EPF Self Contribution.

EPF Self Contribution is open for Malaysian who is existing EPF member.

Since you’re planning to pay through online banking, just remember to select ‘EPF Self Contribution’ from the payment type and most importantly, quote your EPF number. For offline payment, you’ll need to attach with Form 6A(1). Else the payment will become UFO 😛

Some additional information, for EPF i-Saraan (self-employed), there’s an additional registration needed even though the member is existing EPF member due to the government incentive. Please don’t get confused between EPF Self Contribution and EPF i-Saraan ya.

Hope this helps.

Hi Michelle,

Thanks a lot for sharing. My understanding is the maximum per annum would be RM60,000 solely for this extra self-contribution, however, would like to confirm that is it compulsory for me to pay the “EPF Self Contribution” every month with a fixed amount once I started the first pay? For example, I start to pay in January 2021 with RM500. Can I choose not to pay in February 2021 and subsequently RM300 in March 2021?

Hi Chloe,

Thank you for your kind words.

Yes, you’re right – the RM60,000 per year is SOLELY for EPF voluntary contribution scheme including EPF Self Contribution.

Since it is under a voluntary scheme, there’s no compulsory payment or fixed amount for EPF Self Contribution. Under this scheme, you can contribute whenever you are able to do so.

You can also find more details on the EPF website.

Hope this helps and thank you for your comment. It’s great to learn together to build our retirement fund 🙂

Hello there. There is this odd question which I think is relevant. I am self-employed and supposedly can I pay proportionately to my Account 1 and Account 2 just like a normally employed staff?

Thank you,

Jason

Hi Jason,

Yes, as a self-employed, you still can contribute to EPF either through the:

1. EPF Self Contribution or

2. EPF i-Saraan (government initiative specifically for self-employed with 15% matching incentive, up to RM250 per year).

For EPF Self Contribution, there’s no incentive.

Some additional info: For EPF i-Saraan, you need to register (activate) for it at the nearest EPF office (or perhaps you contact the EPF if there’s another way to register for i-Saraan during the pandemic/MCO) before you do a bank transfer so that you are eligible for the gov incentive. Your EPF number for i-Saraan still remain the same.

And for EPF Self Contribution, there’s no registration involved and you can directly do a bank transfer to your EPF account by quoting your EPF number in the transaction slip.

I share about my EPF i-Saraan experience on this blog too. Do take some time to read through. Hope this helps.

Hi Michelle, I am not sure anyone asked this before. Since EPF i-Invest imposes no upfront fees for withdrawal from account 1 for unit trust investments. Is it possible (and sensible) to go for that (MIS scheme) for x amount to enjoy higher returns with low/zero fees, and I self contribute back the x amount (in a lump sum, subject to the maximum of RM 60k) from my bank saving to enjoy the higher return (dividend of EPF) compared to bank FD rate?

Hi Casey, thank you for your comment.

Firstly, no, no one asked me the question before. I am aware of i-Invest but at the moment, I am not participating in i-Invest yet.

I would say, you’ve got your point of contributing back the x amount through EPF Self Contribution to ‘cover’ the amount you plan to invest through i-Invest.

Do take note, although EPF imposes no upfront fees from EPF account 1 for i-Invest, do check for other fees (if any) involves, such as fees by the Fund Management Institutions (initial service charge, exit fee, annual management fee). As these fees can affect the actual returns from your investment. Perhaps, do some calculation whether the returns (after deducting the fees) can outperform the average EPF dividends.

Or, you might want to consider other investment vehicles such as the robo-advisor.

Hope the above help and thanks again for sharing your thought.

Thanks – yes I have taken a simple calculation based on say “fund A” via i-Invest vs investing also in “fund A” via an external/retail entity like a local commercial bank which would charge typically anything from 1-3% of charges, it would seem to be a saving. “fund A” would obviously be something that has already proven its case via positive returns (compared to the usual EFP dividend rate), all other fees being equal, only that risks of “fund A” would be also higher compared to EPF to give the higher returns.

Hi Casey,

Yes, the higher risk of ‘fund A’ compares to the usual EPF dividend rate would be another factor to consider as past performances are no guarantee of future results. Thanks again for sharing your thought.

Hi Michelle, thank you so much for this write-up. So good! Now I understood clearly the process of self-contribution. Just want to ask, do you know when we make payment EPF online, does the system automatically proportion the funds between Account 1 and Account 2 later in the Statement?

Hi Jonathan,

Thank you for your kind words, it means a lot to me. Thank you for your comment as well.

For the EPF fund’s distribution, I checked my own EPF statement based on my i-Saraan contribution, EPF automatically allocates 70% of my contribution to Account 1 and the balance of 30% to account 2. As for the i-Saraan 15% matching contribution, it’s allocated to my EPF Account 1.

Hope this helps.

Thank you so much Michelle. I have made my first self-contribution via Maybank2u two days ago. And yet to see a transaction update in my i-Akaun.

Hi Jonathan,

For your contribution through MBB2U, did you provide the accurate personal details such as EPF number? Or you may call EPF at 03-8922 6000 (8am to 5pm, mon- fri) or contact their official social media channels to check on your deposit.

Do keep a copy of your transaction slip for future reference.

Hope this helps.

Yes, I did provide the correct EPF number. This is worrying. Will call them up on Monday then. Which social media I can check from them?

Hi again, Jonathan.

I understand how it feels. Btw, could the delay in updates of the contribution due to the EPF dividend thing?

If your contribution still not been updated, do call them up on Monday. As for social media, I saw them quite active on Twitter and Facebook. Remember to look for the official social media channels and do not provide personal details to unauthorised personnel.

Hope this helps.

Thanks again Michelle for the good advice.

Hi Jonathan,

Don’t mention it.

Btw, I found on the EPF Self Contribution page, it mentions ‘Up to 14 working days may be needed before the contribution is reflected in your statement’.

Perhaps, update here once the contribution is reflected in your EPF statement.

I think others also curious to know how long before they can see their EPF self contribution reflected in the EPF statement. Thank you.

I’m already retired and what funds I have are in account 55 (whatever that is). Can I also make voluntary contributions to my EPF account?

Hi Greg,

Thank you for your comment. Based on the details on the EPF website the 2 requirements for EPF Self Contribution are:

1. Malaysian Citizen

2. Registered EPF member

It does not mention the age-limit for EPF Self Contribution. Whereas, for the other 3 voluntary EPF contribution schemes, there’s an age-limit:

1. i-Saraan – below 55 years of age

2. i-Suri – below 60 years of age

3. Top-Up EPF savings – Toppee/recipient below 55 years of age

You may want to confirm that by calling EPF at 03-8922 6000 (8 am to 5 pm, Mon- Fri) or write-in to EPF.

Hope the above helps.

Apparently i have may have input wrong epf member account when i did transfer via maybank2u for self contribution

I tried call Maybank but they ask me contact epf to sort out. I called EPF but my call keep getting rejected. Any suggestion

Hi redeye,

Recently I contacted EPF via enquiry/email and the auto reply mentioned to expect some delay in response as EPF is receiving high volume of quiries. I guess that’s why it is hard for the call to get through as well.

You may keep trying to call them at 03-89226000. Alternatively, you may reach them via the EPF inquiry or through EPF official Facebook, Twitter and Live Chat.

Hope the wrong EPF number for your EPF self contribution will be sort out soon.

Well, manage to contact EPF yesterday. They advise to follow up in 3 working days to see if the transaction is successful or not.

Guess a piece of good advice for others is if u make a self contribution via online banking. It is not immediate so you have to wait for at least 3 working days for the deposit to go through. So only call them if u don’t see it within 3 days.

Hi redeye,

Great to know you managed to contact EPF. And thank you for sharing your advice with me and other readers to wait for at least 3 working days for the deposit to be updated/reflected on the EPF statement. This is very helpful info. Appreciate it.

Hope your EPF contribution shall be updated accordingly even though you’ve entered the wrong EPF number.

Hey Michelle

Just a quick update. Just check my EPF. Look like it been updated earlier than scheduled.

Hi redeye,

That’s great to know 🙂

And thank you for updating us here. Appreciate it.

Hi Michelle,

The first payment took quite a few days and you were right, it was because of the dividend thingy. Then I made another payment and it took about 3 days to update. Now I am going to make a payment for the month of March but failed. And it is weird, last payment accepted cents. But this time not accepting any decimals.

Hi again Jonathan,

Great to know your EPF self contributions were updated accordingly.

As for the decimals (cents), I remember both my EPF contributions through Maybank and Public Bank only allowed a rounded amount.

For Public Bank, it clearly stated ‘No sen amount allowed for EPF transactions’.

May I know if your ‘cents’ contribution updated accordingly?

And thanks for updating and sharing your EPF self contribution status.

Hi Michelle,

Thanks for sharing the info. I am a Malaysian who is working overseas but am now in Malaysia. Without doing a proper survey, I did transfer 2 amounts of money from Maybank2U to i-saraan and self-contribution.

However, I just noticed that I need to open the account of i-saraan after reading your article here.

After a few days, I also noticed that no money had been transferred successfully to my EPF accounts. In this case, what should I do to correct my mistake for i-saraan and verify the transaction related to self-contribution?

Thanks for your advice.

Hi Wong,

Thank you for your comment.

For i-Saraan, even though you are an EPF member, you still need to register by submitting Form KWSP 16G(M) so that you are entitled to the benefits such as the matching 15% matching government incentive (max RM250 per year) for the year 2018 until the year 2022.

For my i-Saraan, I registered it at the EPF counter in 2019. You can read my sharing on my other post, EPF i-Saraan: How to register & its 6 benefits.

For EPF self-contribution, there is no registration needed.

If I were you, I would visit the nearest EPF office to:

1. Informed them about the 2 transfers through Maybank2U. In case these transactions still not reflected in your EPF statement, ask the EPF officer for advice.

2. Register for i-Saraan (in case you intend to register i-Saraan for the incentive).

Otherwise, you may want to call EPF or send them an inquiry through the EPF website ‘Connect With Us‘ about the 2 transactions which were not reflected in your EPF statement.

Btw, based on the EPF website, they might take up to 14 days before the contribution reflected in your statement.

Hope the above helps. Perhaps share with me what’s the outcome of your case.

Hi,

For how long(age) we can do the self contribution and Top Up Saving in EPF? What is the rate for these 2 contributions?

Hi Chit,

Thank you for your comment.

Based on the information on the KWSP website:

1. For EPF self contribution, there’s no age requirement mentioned. I assume we can contribute until the maximum age to contribute to EPF, that is 75 years old.

2. For EPF Top Up Savings, the toppee must be below age 55 years old.

3.As for the rate, since these are voluntary contributions, there’s no minimum contribution but the maximum contribution under voluntary contribution is limit to RM60,000 per year.

If you still have doubts, please reach out to KWSP for further clarification.

Hope the above helps.

Hi Michelle,

Thank you for sharing so much useful info on the EPF self contribution. I just wish to confirm that whatever amount we have contributed via self contribution will add up to our Total Balance for us to entitle/enjoy the dividend distribution that to be announced annually by EPF, right? What is the minimum age-eligible to make the withdrawal from these funds? Is it start from age 50? Thank you very much for your reply in advance.

Hi Ching,

Thank you for your comment and your kind words. It means a lot to me 🙂

Yes, the EPF contribution through Self Contribution shall add up to our Total Balance and shall entitle for the yearly dividend distribution.

The withdrawal follows the standard EPF withdrawal as mentioned on the EPF website.

If you still have doubts, please do contact EPF ya.

Hope the above helps 🙂

Thanks for your post. As I’m overseas now and can’t foresee when I’ll be back in the near future, can my parents do the contribution on my behalf, maybe through the EPF counter? Online banking isn’t possible right now for me…

Hi Cindy,

Thank you for your comment.

Based on the EPF website for Self Contribution, it mentions contributors will need to attach KWSP Form 6A(1) for all payments made and didn’t mention it must be the EPF account holder. If you ask your parents to contribute on your behalf at the EPF counter, they must bring along the completed KWSP Form 6A(1) with the cheque.

As for cash, EPF contributors are not encouraged to contribute a large amount at the EPF counter (based on the EPF website remark) the maximum cash contribution at the EPF counter is RM500. Make sure your Name, NRIC and EPF number are correctly written on the KWSP Form 6A(1). The contribution made over the counter also might take up to 14 working days to be reflected on your EPF statement.

Do your parents have online banking? For your information, in 2018, I successfully made an online transfer (from my bank account) to my hubby’s EPF account. You may want to inform your parents to try to make a small contribution, say RM1 to try it out. The online transfer:

1. does not require Form KWSP 6A(1)

2. shall be updated within 3 working days

3. require you to enter your name, NRIC and EPF number correctly

This is just my suggestion based on my experience.

It’s always best to send an official enquiry to EPF to clarify it. Usually, I received their feedback within a few working days.

Hope the above helps and let me know if you have other enquiries.

Thank you for your article. It’s has answered some of my queries.

Hi Wendy,

Thank you for your comment. Glad to know my sharing has answered some of your queries.

If you don’t mind, please share your other queries as well. Then, I can update my sharing for the benefit of other EPF members.

Thank you once again for taking the time to leave a comment on my blog. It means a lot to me 🙂

Hi Michelle,

If I contribute to the self contribution account. When i withdraw the money at age 65, do i need to pay tax on the money I withdraw? And will there any tax on the profit/dividends accumulate each year?

Thanks,

Phil

Hi Philip,

Thank you for your comment.

I’ve never made an EPF withdrawal before. When I asked a family member, he said there’s no tax on the EPF withdrawal he made a few years ago. As for the dividends, no, there’s no tax imposed.

By the way, I found the info published on the EPF website mentioned that there’s no tax on the monies withdrawn from EPF savings withdrawals and returns on investments (dividends). You can find the details on EPF website on Home>Member>Overview, under ‘Your Entitlement’ tab, look for ‘Your Benefits’ and it’s under ‘Tax Exemption’.

Alternatively, you may consider writing to the EPF team by sending them an enquiry online. So far, I’ve received replies to all my questions through the enquiry online.

Hope this helps.

Hi Frank,

Thank you very much for all your great info.

I tried logging into my Maybank online account and can’t seem to find the PAY to EPF icon or site.

Can you please advise?

Thank you.

Daniel

Hi Daniel,

Thank you for your comment and kind words.

To pay EPF through Maybank online/Maybank2U, here is the step-by-step:

1. click on “PAY & TRANSFER” tab

2. click on “PAY”

3. under “Pay To”, look for “EPF” under the “Payee” list

Alternatively, you may refer to my detailed sharing on how to pay EPF through Maybank2U.

Hope this helps. By the way, I am not Frank. I am Michelle, the owner of The Money Magnet blog 🙂

Hi, can I check is the amount of voluntary contribution eligible for tax relief?

when employed, we received 13% epf from employer and 11% employee contribution

and the amount of epf we can claim for tax relief will be the employee portion right

when self-employed and I would like to do the voluntary contribution, is the whole amount I contributed all can claim for tax relief?

Hi Ho,

Thank you for your comment.

Yes, EPF voluntary contributions are eligible for tax relief but the amount is restricted (not all contributions).

For example, for the year of 2022, the eligible amount of LHDN tax relief (employee contribution only or self-employed) under EPF is restricted to RM4,000 only.

If you’ve contributed RM10,000 to EPF for 2022 through the voluntary contribution scheme, your can only claim RM4,000.

You may refer to the tax relief details on LHDN website.

Hope the helps.

Good evening!

Being housewife for 30 years, now of age 55. Had never contributed any amount only until recently just contributed into I-Saraan account. I wish to make another contribution into my EPF account. Should I transfer into I-Saraan or Self Contribution?

Hi Jenn,

Good morning!

Thank you for your comment and apologize for late reply.

Since you are a housewife and had registered and contributed into i-Saraan, you may continue making contribution through i-Saraan. Also, for the year of 2023, the i-Saraan matching 15% special incentive has been increased to a maximum of RM300 instead of the previous years of RM250. FYI, I contributed RM2000 into my i-Saraan earlier this year and I’ve recently saw the RM300 government incentive credited into my EPF account.

For additional information, i-Saraan contributions age limit is below 60 years of age. So, you’re still eligible to contribute to i-Saraan. Do take note that EPF contributions made after the age of 55 will be parked under EPF Akaun Emas. And you can only make withdrawal from Akaun Emas once you reach 60 years old.

BTW, you may read more about the scheme in my other blog post about i-Saraan. You may also visit KWSP website and chat with chatbot or call to KWSP hotline for further details.

Hope the above helps. Feel free to let me know if there’s anything unclear.