This post is on EPF i-Saraan aka KWSP i-Saraan (previously known as the 1Malaysia Retirement Savings Scheme (SP1M)).

I first wrote this post back in 2018 after my husband and I registered for i-Saraan in 2018 and 2019 respectively.

I thought it would be a good idea to share our experience on the i-Saraan scheme so that others (especially self-employed) are aware that they too can contribute to EPF.

Since then, I tried my best to update the information on this page to include the latest changes and updates.

Table of Contents

- What is i-Saraan?

- i-Saraan eligibility

- i-Saraan registration

- How to make an i-Saraan contribution payment?

- i-Saraan contribution limit

- 6 i-Saraan benefits

- When will I receive the 15% i-Saraan contribution from the government?

- How to register as an EPF member?

- Final thoughts

What is i-Saraan?

Generally, all employees in Malaysia are aware that they must contribute to EPF (Employees Provident Fund) or locally known as KWSP (Kumpulan Wang Simpanan Pekerja).

Their employers will deduct the EPF contribution amount based on their salary range. And then submit these contributions to EPF together with the employer’s EPF contribution on a monthly basis.

Other than this mandatory requirement by the EPF Act 1991, the EPF also encourages its members to contribute through various voluntary contributions schemes made available from time to time.

Among the top initiatives are voluntary contributions from:

- self-employed individuals

- salaried workers

Self-employed individuals may contribute through the i-Saraan or Self Contribution scheme while salaried workers may make additional contributions through the Self Contribution scheme.

With that said, i-Saraan is an EPF voluntary contribution created especially for those who are self-employed. And there is a government incentive to encourage self-employed individuals to contribute to their EPF savings.

The details of the i-Saraan government incentive are as below:

- eligible for a 15% matching incentive from the government.

- government incentive is subject to a maximum of RM250 in a year (2018 to 2022), RM300 in a year (2023), RM500 in a year (2024).

- the incentive is for members below 60 years old only (previously, were below 55 years old).

- the incentive is from the year 2018 to the year 2022 and has been extended to 2024.

As for EPF Self Contribution, it is a voluntary contribution where all EPF members including self-employed and salaried employees may make additional contributions to their EPF savings.

If you wish to know more details about EPF Self Contribution, you can read my other post on EPF Self Contribution. The post also come with description of differences between i-Saraan and Self Contribution: i-Saraan vs EPF Self Contribution

i-Saraan eligibility

Individuals who are self-employed and not receiving a fixed income are eligible to register for i-Saraan.

Some examples of those who fall under the self-employed category may include the following:

- Photographers

- Hairstylists

- Tutors

- Farmers

- Fishermen

- Taxi drivers

- Swimming instructor

- Independent gig workers (e-hailing drivers such as Grab, e-commerce delivery such as Shopee agent)

- Bloggers, Youtubers, influencers, and content creators

- Hawkers and night market traders

- Insurance agents, real estate agents, unit trust consultants

- Freelance workers (deejays, singers, actors, fitness instructors, and consultants)

- Business owners (sole proprietors or partnerships)

- Professionals with their own practice (accountants, doctors, dentists, lawyers)

- Housewives

- Baby sitters

- Pensionable employees

In other words, a Malaysian who is not an employee is eligible to apply for the i-Saraan scheme.

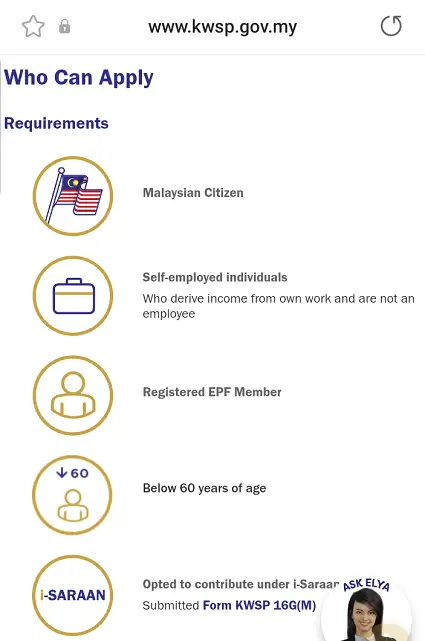

As stated in the EPF website screenshot above, the criteria to register for i-Saraan are as below:

- Malaysian citizen

- Self-employed individuals

- Registered as an EPF member

- Below 60 years of age (Previously was below 55 years of age)

- Has opted to contribute under the i-Saraan (previously known as the SP1M) by submitting Form KWSP 16G(1M)

Thus, do take note that if you are an employee who receives regular income, you are not eligible to participate in the i-Saraan scheme.

For sharing purposes, both my husband and I are eligible for i-Saraan. My husband is a small business owner and I am a content creator on this blog, The Money Magnet.

Read more: Can we rely on EPF savings to fund our retirement years?

i-Saraan registration

Back in 2018 and 2019, my husband and I registered our i-Saraan at the EPF office in Kuching.

As of the time of writing, EPF members can also register i-Saraan online or through the EPF kiosk.

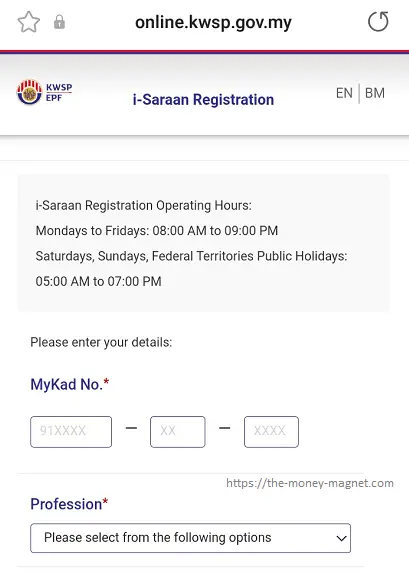

i-Saraan online registration

For online registration, you may visit the i-Saraan online registration website.

Below is a screenshot of a part of the i-Saraan online registration form.

Then, you’ll need to fill in the form accordingly. Do take note of the i-Saraan online registration operating hours.

Since I am already a registered i-Saraan member, I can’t try out the online registration.

If you’ve tried online registration, perhaps share your experience in the comment below. I believe this will help other readers who are keen to register for i-Saraan online.

Personally, I think the online i-Saraan application is such a helpful initiative. It is convenient, fast and hassle-free for EPF members to submit their i-Saraan application online.

i-Saraan registration at the EPF office

Other than the online registration above, you may register for i-Saraan at the EPF office as well.

The sharing below is based on my husband and my experience registering our i-Saraan at the EPF Kuching office in 2018 and 2019.

1. Obtain KWSP Form 16G(M)

Interested individuals can apply by submitting KWSP Form 16G(M) – Application for Self-contribution (Government Incentives – i-Saraan/i-Suri).

The form is available from the nearest EPF branch office. It is free of charge.

Alternatively, you can download KWSP Form 16G(M)(PDF) from the EPF website. But, I would advise getting the form while you are at the EPF counter in case they have an updated version.

Please take note, even though you are an existing EPF member, you still need to register for i-Saraan by submitting KWSP Form 16G(M).

2. Fill up KWSP Form 16G(M)

Next is to fill up the form. When my husband and I filled up the form in 2018 and 2019, the form consists of two pages.

But the applicant only needs to fill up the first page. Which, consists of the applicant’s personal information and contact information.

While the second page consists of the guideline on how to fill up the form.

3. Submit KWSP Form 16G(M) to EPF

Lastly, submit the form by hand or by post to your nearest EPF branch office. I highly recommend interested individuals submit the form by hand to the nearest EPF branch office.

Because at the same time, you can get a ticket number and complete the submission immediately over the counter.

Do bring along a copy of your NRIC too.

Once completed, the EPF officer will print out the EPF i-Saraan confirmation notice. The applicant will get a copy of this confirmation notice as well.

Then, the applicant can immediately make his contribution to i-Saraan.

For my husband’s application, he submitted the form over the counter at the EPF Kuching branch. It took him about 30 minutes to complete everything.

As for me, I took about 25 minutes to register my EPF i-Saraan at EPF Kuching Branch.

For the latest procedure for submitting the form, do consider calling or contacting your nearest EPF center.

How to make an i-Saraan contribution payment?

According to the EPF website, members can make their contribution payments via the channels below.

Do take note to mention the payment is for i-Saraan contribution to ensure you are eligible for i-Saraan benefits such as the government incentives.

1. Mobile app

For payment via the EPF Mobile app i-Akaun, members may complete the transactions through FPX. The minimum contribution through Mobile app i-Akaun is RM10.00.

You can find more details including screenshots on the EPF website.

2. Internet Banking

Secondly, you make your i-Saraan contribution through online banking at the following participating banks:

- MBSB Bank

- MAYBANK (M2u)

- RHB Bank

- PUBLIC BANK

- Bank Muamalat

- Alliance Bank

- Hong Leong Bank

- Bank Islam

- Cimb Bank

Please refer to the official EPF website for the updated list of participating banks.

3. Bank agent counters

Thirdly, you may pay for your EPF contribution through selected bank agent counters:

- Bank Simpanan Nasional (BSN)

- Maybank

- Public Bank

- RHB Bank

Please refer to the official EPF website for the updated list of bank agent counters.

And please submit your contribution with a completed Form KWSP 6A(2). This is important to ensure the payment updated accordingly.

4. Registered Bank Agent

You may also pay your i-Saraan contributions through BSN Bank Agent (Ejen Bank Berdafter (EBB) BSN).

For this option, do remember to attach with a completed Form KWSP 6A(2) .

5. EPF counters

Lastly, you may make your i-Saraan contribution by cash (maximum RM500) or cheque at the EPF counter with Form KWSP 6A(2)(PDF).

How to pay i-Saraan via online banking?

My husband made his first contribution through Public Bank online.

Earlier on, the EPF officer also handed him a simple but useful step-by-step guideline on making contributions through online banking.

In case you wish to know the procedure for making a self-contribution through Public Bank online banking, the site by step is as below:

- Log in to Public Bank online banking (desktop view)

- Select Payment

- Choose Other Payment

- Then select EPF Payment from the options

- Followed by selecting Account & Payment Type (Bayaran Caruman Pilihan Sendiri or Bayaran caruman i-Saraan / i-Suri)

- At this step, make sure you choose Bayaran caruman i-Saraan / i-Suri

- Fill in details (Member’s Name, Member’s EPF No., Member’s NRIC No., Contribution Month, and Contribution Amount)

- Request PAC Now

- Confirm the transaction

Once the transaction is completed, do keep a copy of the transaction slip for future reference.

As for me, I made my EPF i-Saraan contributions through Public Bank online and Maybank2u. I also share the step-by-step with screenshots on how to make an EPF contribution online.

You can read the details in my sharing below:

If you wish to make EPF i-Saraan payment through Public Bank or Maybank, do have a look at my sharing above.

One important thing is to remember to choose ‘i-Saraan / i-Suri‘ from the ‘Type of EPF payment’ drop-down menu.

If you accidentally select ‘Self Contribution’ or ‘Bayaran Caruman Pilihan Sendiri‘, you will not receive the matching 15% government incentive. You will need to contact EPF for correction before they can credit your EPF account with the incentive.

i-Saraan contribution limit

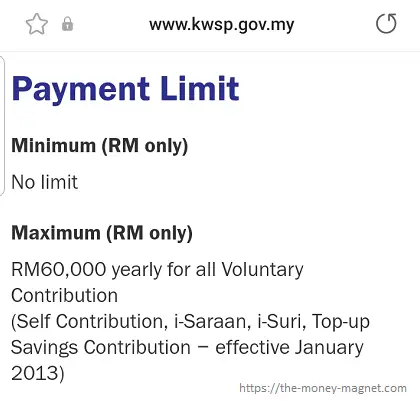

Even though EPF highly encourages self-employed individuals to make voluntary contributions, there is a contribution limit as per the screenshot below.

Further explanation is as below.

1. Maximum voluntary contribution of RM60,000 per year

Currently, there is a maximum payment limit of RM60,000 yearly for voluntary contribution schemes.

To put in other words, a member is not allowed to contribute more than RM60,000 in a year under voluntary contribution, including EPF i-Saraan. Do take note the RM60,000 is excluding the contribution from mandatory contribution through employment.

With that said, the maximum i-Saraan contribution is RM60,000 per year, including other voluntary scheme sucsh as EPF Self Contribution and Account 1 Top-Up Savings.

(For those above 55 years old, your EPF contributions made between 55 to 60 years old will be parked under a separate account, Akaun Emas. And you can only make withdrawal from Akaun Emas at 60 years old.)

2. No minimum contribution is required

As for the minimum contribution amount, i-Saraan has no minimum contribution required except the RM10.00 for contributions made through Mobile app i-Akaun.

Read more: How to check your EPF number?

6 i-Saraan benefits

Here are the 6 benefits of contributing to i-Saraan:

1. Eligible for a 15% government incentive

Members aged below 60 years old who made a self-contribution through the i-Saraan scheme shall receive a government contribution of 15% of the amount contributed. This government incentive is subjected to a maximum of RM500 a year for the year of 2024.

To reap the RM500 matching incentive, all you need to do is to contribute RM3,334 through i-Saraan.

For any further extension of the incentive, I’ll update this post. Alternatively, you may refer to the EPF website for the latest updates.

2. Enjoy Annual EPF dividends

Savings under the i-Saraan scheme shall receive EPF annual dividend payments credited to their account up until the member reaches age 100.

As announced in 2023, the EPF dividends for 2022 are at 5.35% for Simpanan Konvensional and 4.75% for Simpanan Shariah. These dividends are considered very attractive.

And for your information, EPF guarantees a dividend of 2.5% per year for its member’s savings.

3. Eligible for LHDN income tax relief

The third benefit would be the eligibility for income tax relief.

For the assessment year 2022, the tax relief for EPF contribution and other approved schemes is up to RM4,000.

I believe many self-employed individuals in Malaysia are not aware that they can register as EPF members and start contributing through the EPF i-Saraan scheme.

Thus, they missed out on the opportunity to maximize their income tax saving through EPF contributions.

4. Eligible for EPF death benefit of RM2,500

In 2019, I also contacted EPF through their website to ask whether an EPF member under the i-Saraan scheme is eligible for the death benefit of RM2,500.

The answer is “Yes”, provided they fulfill the terms and conditions of EPF withdrawal.

5. Flexible EPF contribution

Another benefit of the i-Saraan scheme is the flexibility to make contributions in terms of:

- contribution amount

- the member may make any contribution amount within his or her own financial ability.

- contribution frequency

- the member may make the contribution anytime according to his or her own timing and schedule.

The flexibility offered is a great advantage for self-employed individuals as they can contribute according to their own financial capabilities.

6. To improve your credit score

Lastly, contributing to EPF i-Saraan may also improve your credit score.

Perhaps in the future, you may want to apply for loans such as housing loans. The regular EPF contributions which you have made throughout the years are a sign that you are a committed and responsible person. Thus, this may make the loan approval smoother.

Personally, I had come across a credit card company that uses EPF statements to support my credit card application.

So, making regular EPF contributions may boost your credit score.

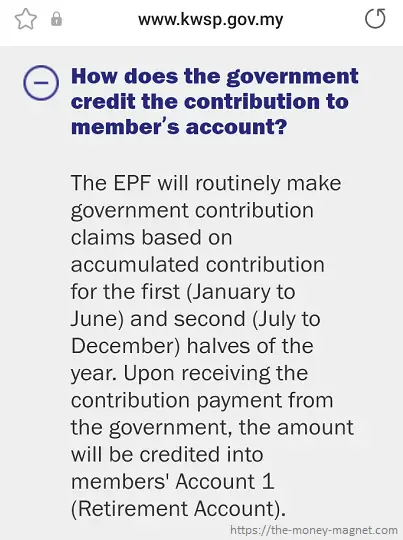

When will I receive the 15% i-Saraan contribution from the government?

Based on the EPF website, the EPF team will routinely credit the government incentive to the i-Saraan account holders. The amount shall be based on the accumulated contributions made for the first and second halves of the year.

You may refer to the screenshot below.

As for me, I received the 15% i-Saraan contribution from the government for all the contributions I made in 2019.

For the contribution I made in the first half of 2019, I received a 15% contribution from the government in the last quarter of 2019.

The screenshot from my EPF i-Akaun is as below:

While for the contribution I made in the second half of 2019, I received the 15% incentive in the first quarter of 2020.

I share the print screens from my EPF i-Akaun below:

Do take note the 15% matching i-Saraan contribution from the government is under ‘Pelarasan dan caruman tertunggak‘ as shown in the above print screen.

As of 2023, I’ve received all the 15% matching government incentives credited into my EPF account.

How to register as an EPF member?

If you have been self-employed all this while, most probably you haven’t registered as an EPF member.

But, don’t worry because you can easily register as an EPF member through either one of the methods below:

1. Registration EPF at the counter

You can register as an EPF member through the counter at your nearest EPF branch office.

Bring along your MyKad for verification purposes.

Once successful, you will receive a notice with your EPF number stated.

2. Registration EPF through EPF kiosk

Besides registration at the counter during working hours, you also can register as an EPF member through EPF self-service kiosks.

These EPF kiosks are available at the EPF branch office nationwide. Some of these kiosks are available after working hours.

You may refer to the EPF website for a complete list of nationwide EPF kiosk locations. All you need to do is to bring along your MyKad to your nearest kiosk. Then, just follow the instructions accordingly.

Upon successful registration, the member will receive a notice with the EPF number.

Final thoughts

With the above, I hope you have a better understanding of the EPF i-Saraan scheme, including how you can start contributing, and its 6 benefits.

If you have friends or family members who are self-employed, perhaps you can share with them on the i-Saraan retirement scheme. Maybe they are not aware of this EPF scheme which can help them to reap many benefits including the government incentive.

Let’s help each other to secure bigger EPF savings for better retirement years.

For the most updated information on the voluntary retirement scheme, please visit the official EPF website.

If you have any other things you wish to know about i-Saraan, please leave your comment below.

Lastly, feel free to read my other post on EPF, retirement planning and learn how to grow your retirement fund through various investments.

Can we still contribute in i-Saraan if we are working overseas?

Hi Bluey,

Apologize for the late reply. Yes, Malaysian working overseas still can contribute to i-Saraan.

They will need to register themselves as EPF member first by submitting Form KWSP 3.

You can read more details EPF website.

For news on whether Malaysian working overseas can register for EPF, you can read the news on The Star Online.

Hope the above helps.

May I know whether need to submit documents to prove the occupation for i saraan application?

Hi John, thank you for your comment. When my husband registered his i-Saraan in Dec’18 and I registered mine in Jan’19, there is no docs or proof needed for the occupation type.

Thanks for the informative post! I’ve read on http://www.kwsp.gov.my/member/contribution/i-saraan that the allowed tax relief is RM4,000, would you happen to know if this is a separate tax relief, or if it limits the tax relief of EPF to RM4,000 only instead of the usualy RM6,000 if you go under I-Saraan?

Thanks!

Hi Mel, thank you for your kind words. With regards to the tax exemption, I have already sent an inquiry to the EPF team. I am waiting for their reply. On EPF old portal (I noticed they had recently upgraded their EPF portal), the tax relief is the same (up to RM6000 in combination with life insurance) for all type of contribution, no separate tax relief for i-Saraan contribution.

Once I received their feedback, I shall update here again.

Hi again Mel,

EPF team replied to check with IRB on the tax exemption. Then, I recalled that in Budget 2019, there was a new structure for EPF and life insurance tax relief. From my further checking, found out that for 2019, the government proposed to separate the previously combined RM6000 tax exemption for both EPF and life insurance to RM4000 for EPF and RM3000 for life insurance/takaful. You can read more details on The Star Online.

As for the i-Saraan, from my understanding, there is no separate tax relief for the i-Saraan contribution. The tax exemption of RM4000 as mentioned on the EPF website is for all contributions to EPF. Further details on tax exemption up to the year 2018 as listed on the LHDN website.

Btw, thank you for asking this question. Else, I might miss out the new structure for EPF and life insurance tax exemption for YA 2019 🙂

Hi, I wish to know this few years I already go Maybank2u to contribute as self contribute. If I choose contribute for i-saraan, should I thru online contribute or must fillup form and direct hand to EPF office?

Maybank2u show 01. self contribute 02. i-saraan/i-suri

Thanks

Hi Lian Leng, eligible EPF member needs to register for EPF i-Saraan. Even though you already an EPF member, you still need to apply for i-Saraan. If you are not registered under i-Saraan, you will NOT entitle for the government contribution. Only after register for i-Saraan, you can contribute i-Saraan through online banking such as Maybank2u. In 2018 and 2019, my husband and I personally went to the EPF office for the i-Saraan registration.

So, firstly, get your i-Saraan application approved. Secondly, contribute through Maybank2u by choosing 02. i-Saraan/i-Suri. Hope this helps.

Hi Michelle, that’s mean I have to go EPF office and cannot apply online.

Yesterday EPF office just start work, tomorrow should be a lot of people.

Hi again Lian Leng, I suggest you call EPF at 03-89226000 (8 am-6 pm, Monday – Friday) to ask them whether you can apply i-Saraan online. Or, drop them a message through EPF Connect With Us.

Hi, Can I apply for a housing loan with i-saraan contribution? Because I’m not working. I’m an online seller. Please guide.

Hi Yuvarani,

Thank you for your comment.

As per my sharing above on EPF i-Saraan, those self-employed are eligible to register for EPF i-Saraan.

So, if you’re not an employee who contributes the mandatory monthly EPF contribution, you are eligible to register for EPF i-Saraan.

And as for the housing loan, your contribution through EPF i-Saraan will go to the EPF account.

So, the housing loan also follows the EPF withdrawal for housing loan eligibility and rules.

Hope my explanation above helps. Else, please reach out to the official EPF channel.

Hi Michelle. I would like to ask on behalf of my son who is 15 years old and he earns some money monthly by selling products online. Can he register for i-Saraan?

Hi Lisa,

Thank you for your comment.

Based on the 5 requirements for the i-Saraan scheme, I think your 15-year-old son is eligible for i-Saraan (the minimum age to register as an EPF member is and start contributing is 14 years old. You can read about it in my other post on EPF Self Contribution). Do make sure he registers himself as an EPF member first before submitting the i-Saraan Form KWSP 16G(M) either online or walk-in to the nearest EPF office.

I would still suggest you call or send an official online enquiry to the EPF team for confirmation before making a contribution. I would appreciate it if you can share the answer with me.

Btw, it’s really great to know your teenage son is already making money online and saving for retirement at such a young age. This is something to be proud of! Keep up the good work!

Hi,

I’m jobless for 1 year now.

I’m selling my house and wondering if some of the money, I can deposit into EPF for a better return.

If yes, is it under I-Saraan or normal?

Btw, I’m 53 years old now.

Many thanks

LAN

Hi Langes,

Thank you for your comment.

Since you are 53 years old and currently not making an EPF contribution as an employee, you are eligible for i-Saraan (i-Saraan is for Malaysian 55 years old and below).

Through the i-Saraan, you’re eligible for the incentive. So, you may consider registering for the i-Saraan.

Once you’re employed and contributing to EPF as an employee, if you want, you may make continue to make voluntary contributions through EPF Self Contribution to take advantage of the dividend offered. For EPF Self Contribution, no registration is needed.

Do take note, the maximum amount you can contribute through voluntary contribution including i-Saraan and Self Contribution is RM60,000 per year.

Hope the above helps and may you’ll land on a great offer soon.

Hi Michelle,

Good job & good info for me.

I am just wondering, for the i-Saraan or EPF self contribution scheme once registered it must be contributed each month?

Can it be contributed off and on?

Thank you.

BR,

Ng

Hi Ng,

Thank you for your kind words.

Both i-Saraan and Self Contribution are voluntary contributions. This means:

1. You don’t have to contribute each month

2. You can contribute on and off

You may refer to the details of Voluntary Contributions on the EPF website.

Some additional info:

1. EPF i-Saraan – You need to register online/offline even though you are already an existing EPF member (to be eligible for the government incentive)

2. EPF Self Contribution – You no need to register (again) if you are already an existing EPF member

Hope this helps.

Do let me know if you have other questions. Thank you.

Hi, first of all, this is a great sharing, thanks.

I do have a question around the RM60,000 yearly limit, is it based on a calendar year or a year from the first self contribution?

For example, if my first contribution is April 2022, is the limit confined between April 2022 – March 2023? Or Every January the limit gets refreshed.

Thanks.

Bert

Hi Bert,

Thank you for your comment and kind words.

The RM60,000 contribution limit for all EPF voluntary contributions (Self Contribution, i-Saraan, i-Suri, Top-up Savings Contribution) is based on a yearly basis (from 1st January to 31st December).

You may find more information on the EPF Self Contribution website.

Alternatively, you may send your enquiry to EPF online.

Thank you very much for sharing the very useful information. If a housewife has never been employed before (NOT an existing EPF member), can she register herself for i-Saraan? Thank you in advance for your further information.

Hi HN Lee,

Thank you for your comment and kind words.

If a housewife has never been employed before and is not an existing EPF member, she needs to register as an EPF member first. When she has her EPF account number, then, she can proceed to register/opt-in for i-Saraan (either online or at the EPF counter).

To register as an EPF member, she can register at the EPF counter or at EPF Kiosk. Remember to bring along her NRIC.

You may find further details on the EPF website on becoming an EPF member.

In short, register as an EPF member first, then register for i-Saraan.

Hope the above helps.

Hi,

Well done in this very informative website! May I know if I can contribute for Self contribution and I-Saraan at the same time?

Thanks

Emily

Hi Emily,

First of all, apologize for the late response. And thank you for your kind words 🙂

I don’t see the reasons to contribute to both EPF schemes at the same time. May I know your reasons?

In my opinion: If I am eligible for i-saraan, I would contribute to i-saraan because i-saraan comes with government incentive. Else, I may choose to contribute through EPF self contribution.

Let me know if you are ok with my reply 🙂

Hi Michelle,

I found all of your contents and information are very useful and easy to understand! Thanks for sharing! I would like to ask how can i know if i have successfully registered in i-saraan? I submitted the registration few days ago for now I-Akaun are all under maintenence. Cannot even check the status. But just wondering there will be showing I am registered i-saraan somewhere in the app? Or once I contributed, will have to wait and check the upcoming incentives to see if i get 15% incentives?

Hi Sammy,

Thank you for your comment and sorry for late reply.

For my case, as I registered at EPF counter back in 2019, the officer did mention I am eligible for i-saraan and I can start contributing (I think they refer to my EPF statement where I don’t have the monthly mandatory contribution by Employer and employee. I left my full-time employment back in 2018).

As for i-Akaun, I just login and I found out that, you can refer to:

https://iakaun.kwsp.gov.my/portal/member/profile

Under ‘Produk’, it is stated ‘i-Saraan’ for my i-Akaun.

You may try to login and check it out yourself. Yesterday you not able to login, probably due to the EPF Dividend announcement. Else, you may try to call to EPF centre or use the live-chat during office hour to chat with the EPF officer.

If you wait to the upcoming incentives, you may need to wait until after June 2024.

Hope the above helps and appreciate your kind words 🙂