In this Stashaway Simple review, I’ll share my experience and thoughts on Stashaway Simple.

This includes the benefits of StashAway Simple, its drawbacks, other things worth knowing about the cash management solution, and its comparison with Fixed Deposit.

I’ll also include my StashAway Simple returns.

Table of Contents

- What is StashAway Simple?

- 6 Benefits of StashAway Simple

- 3 Drawbacks of StashAway Simple

- Other things worth knowing

- StashAway Simple vs Fixed Deposit

- Who is StashAway Simple suitable for?

- StashAway Simple onboarding procedure

- StashAway Simple returns (2024)

- Final thoughts

[Disclaimer: I am not a certified financial planner. My sharing is purely based on my own research and personal experience. To make the best financial decision that suits your own needs, you must conduct your own research and seek the advice of a certified financial planner if necessary]

What is StashAway Simple?

StashAway Simple is a cash management solution by StashAway, a Robo-advisor platform headquartered in Singapore with offices in other countries including Malaysia.

If you are new to StashAway Malaysia, it is a licensed financial technology (fintech) operator under Digital Investment Manager (DIM) from the Securities Commission Malaysia (SC). StashAway launched its services to Malaysians in 2018.

You can read more about StashAway Malaysia in my StashAway Malaysia review. In the review, I shared my StashAway Malaysia journey, its portfolio performance, and a 50% discount fees promo link for new users.

In 2020, StashAway launched StashAway Simple, a cash management solution that gathers and puts investors’ money in a selected money market fund.

Personally, I would think StashAway Simple is a financial tool with the combinations of some of the following:

- low-requirement savings account

- high-interest savings account

- average fixed deposits placement

As you read further, you’ll see why I think StashAway Simple is a combination of some of the above.

6 Benefits of StashAway Simple

In mid-2021, I made an RM1,000 deposit to my StashAway Simple account. My main objective is to experience it myself if the cash management solution can give me better returns compared to my savings account and fixed deposits.

Before I tried out StashAway Simple, I took the time to explore and understand more about the cash management tool.

From there, I discovered the benefits of StashAway Simple as below:

1. Potential of better returns for my savings

When I first wrote this post in mid-2021, StashAway Simple offers a projected return of 2.4% per annum (p.a.) for whatever balance in my StashAway Simple account.

At that time, the projected return of 2.4% p.a. is much better compared to:

- my fixed deposits placement which is at around 1.5% p.a.

- my normal savings account at 0.20% p.a.

Let’s use a simple calculation to see the difference in the returns.

- Savings amount: RM50,000

- Savings period: 1 year

- Potential returns:

- StashAway Simple projected returns at 2.4% p.a.: RM1,200

- Fixed Deposit at 1.50% p.a.: RM750

- Savings Account at 0.20% p.a.: RM100

From the simple calculation above, the potential returns can be quite significant.

But, it is worth noting that the StashAway Simple 2.4% p.a. is a projected return. This means the actual returns can be lower or higher than 2.4% p.a., depending on economic conditions.

Do take note that, StashAway may revise the projected return rates from time to time. As of the time of this update, StashAway Simple’s projected return is at 3.8% p.a.

For the most updated projected return rate, please refer to official StashAway Simple website.

2. Affordable cash management solution

Unlike most financial tools which require a minimum deposit, StashAway Simple is affordable because there is no minimum deposit.

I am a person who feels comfortable putting more into savings (or investments) after I try out the platform myself. Since I can start with any amount, I am more than willing to try out the cash management solution.

Thus, I decided to try out with RM1,000 to see if I really can enjoy a projected return of 2.4% p.a.

3. Flexible to make withdrawals anytime

Another benefit of StashAway Simple is the flexibility to make a withdrawal anytime and still enjoy the projected returns. This flexibility is similar to the high liquidity offered by a savings account.

Since there’s no minimum lock-up period, I don’t have to worry about losing parts of the returns in case of emergency withdrawal.

This means I have the freedom to withdraw the fund from my account anytime I want.

4. No other investment requirements

For most traditional fixed deposits, the bank usually has certain requirements to enjoy a better interest rate. Such as requiring me to invest a certain percentage of my savings in selected unit trust funds.

Or, I might need to opt for longer fixed deposit tenure with a higher minimum placement.

For StashAway Simple, there’s no other investment requirement needed to enjoy the projected return of 2.4% p.a.

5. A convenient and time-saving financial tool

Similar to other fintech platforms, StashAway Simple is fully digitalized. The whole journey is completed online either through the web or the app.

This includes:

- onboarding process

- making a deposit

- making a withdrawal

- monitoring the cash management

With everything completed online, I am happy because:

- I save time and the trouble of physically visiting the center

- I can access my account anytime – depositing, withdrawing, monitoring

It is a real advantage to have the option to engage a financial tool to grow my cash especially now in the current pandemic situation where movement and contacts are limited.

6. Save on certain fees

This might be minimal but I think it is still worth mentioning. StashAway Simple does not have platform or service fees such as:

- set up fees such as registration or deposit fees

- management fees for any balance in StashAway Simple

- exit fees such as withdrawal fees

Without paying the above fees, I can get more from my savings.

But, do take note that there’s a net fee of approximately 0.5% charged by the underlying fund manager, embedded in the projected rate.

3 Drawbacks of StashAway Simple

In this StashAway Simple review, I’ll also list the drawbacks of StashAway Simple.

1. Capital is not guaranteed

Unlike a fixed deposit placement where the principal is protected, the fund in StashAway Simple is invested in a selected money market fund.

As we all know, all investments involved some degree of risk.

So, the capital is not guaranteed.

Although the capital is not guaranteed, it is worth noting that StashAway Simple underlying investment is relatively low risk with a StashAway Risk Index of 0.1%. This means I have a 99% of not losing more than 0.1% of my Asset under management (AUM) in a given year.

As of the time of writing, my savings in StashAway Simple is 100% invested in Eastspring Investments Islamic Income Fund.

2. Returns are not guaranteed

As mentioned earlier, StashAway Simple’s 2.4% p.a. is a projected return. This means the actual return may be higher or lower than 2.4% p.a. depending on the economic conditions.

Personally, this is not a concern due to the no lock-in period. If I found a better way to grow my money, I can always make a withdrawal anytime I want.

3. Deposit not protected by PIDM

Since StashAway is not a Perbadanan Insuran Deposit Malaysia (PIDM) member bank, my deposit in the cash management solution is not protected by PIDM’s Deposit Insurance System (DIS).

So, if anything happens to StashAway, I do not get the PIDM automatic protection. But, StashAway assures that investors will always have full access and claim to their assets no matter what happens to StashAway.

You can read about it in StashAway Security FAQ.

To be fair, other financial products under unit trusts, stocks, and shares are also not eligible for PIDM protection.

By the way, do you know well about PIDM protection such as under what conditions your deposits are eligible for protection? Find out the details in my other post, PIDM Protection Benefits.

Other things worth knowing

In this StashAwy Simple review, I’ve also compiled a list of other things worth knowing about the cash management solution as below.

1. Approved by SC

I mentioned earlier that StashAway Malaysia is approved by SC. Thus StashAway Malaysia follows the guidelines and requirements of SC.

Among the requirements that I recognized is below:

- Submitting my NRIC and Proof of Residence through the KYC process during onboarding.

- I can only deposit from my own bank account in compliance with Anti Money Laundering Act (AMLA).

- My deposit was transferred to the Pacific Trustee bank account, an SC-licensed trustee instead of the StashAway Malaysia bank account.

As an investor, I feel safe knowing that my money is with an SC-licensed financial institution.

2. Shariah compliance

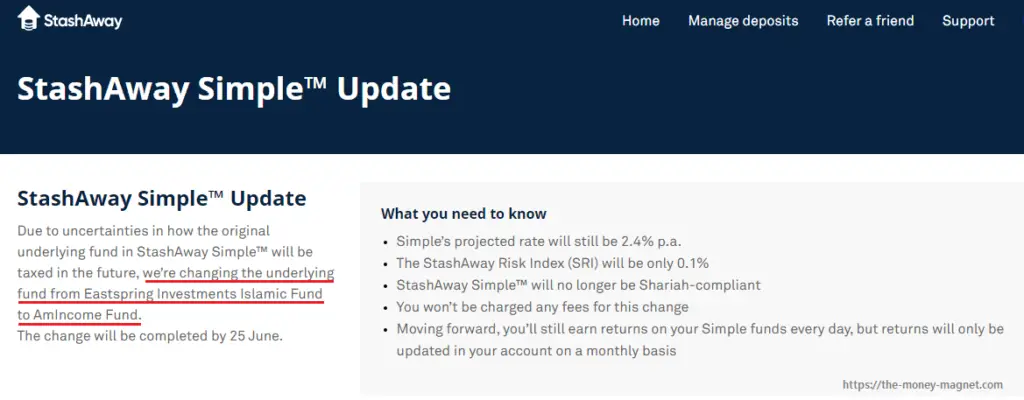

When I started my StashAway Simple cash management back in mid-2021, StashAway Simple was Shariah-compliant. The underlying fund was Eastspring Investments Islamic Income Fund.

One month later, I received an email from StashAway informing me they are changing its underlying fund to AmIncome Fund which was not Shariah-compliant.

When I logged into my StashAway, I saw the notice on StashAway Simple update as below.

As of the time of this update, StashAway Simple underlying fund is back to Eastspring Investments Islamic Income Fund.

Although this does not affect me, I am sharing this for investors who choose to only invest in Shariah-compliant financial services.

For the latest updates on its underlying funds, it is best to refer to StashAway Simple website.

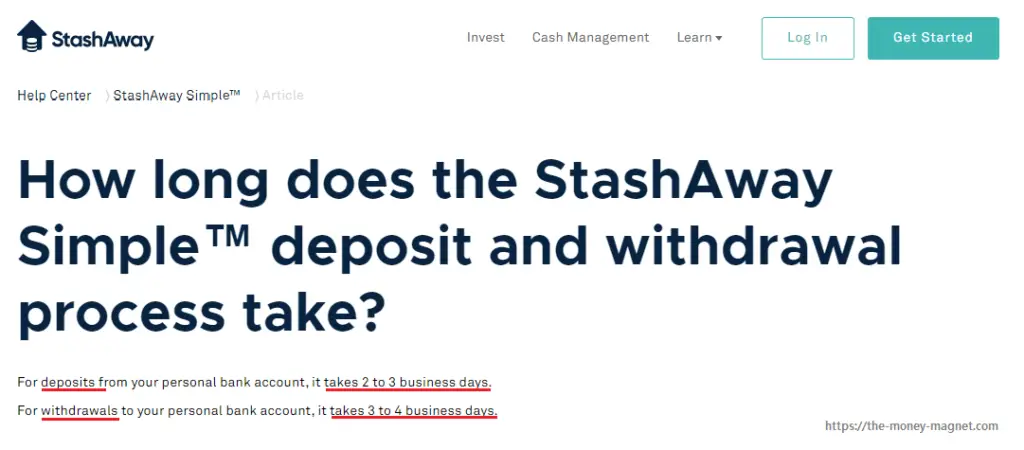

3. Deposit and withdrawal timeline

Based on StashAway Simple FAQ, deposits from a personal bank account take 2 to 3 business days. While withdrawals to a personal bank account take 3 to 4 business days.

From my own experience, I deposited on a Wednesday at around noon. The next day, at around noontime, I received an email from StashAway, mentioning they received my fund and will start the process to invest it.

When I logged in again three days later (Saturday), I saw the deposit reflected in my StashAway account.

As for withdrawal, I have not made any yet. I’ll share it here once I’ve had my withdrawal experience.

I believe the timeline is important so that I can plan the withdrawal accordingly. This is to avoid situations where I need the money immediately but am not aware that StashAway requires 3 to 4 business days before seeing the amount in my bank account.

4. Auto-deposit feature

Similar to the StashAway portfolio, you may also choose to use the auto-deposit feature to allocate funds to StashAway Simple.

This feature is especially helpful for those who prefer to automate their investments or savings. On top of that, auto-deposit may help to optimize your investment through the dollar-cost averaging method.

I find the StashAway article on dollar-cost averaging helpful and worth reading.

5. Unlimited transfer between StashAway portfolios

I’ve also learned that I can make unlimited transfers between my StashAway portfolios.

This means I can make fund transfers between my StashAway portfolios without worrying about the restriction or being charged.

The unlimited transfer feature definitely makes life easier for existing StashAway Malaysia customer who needs to transfer their money to and from their StashAway portfolios.

6. Interest accrued daily

StashAway Simple’s interest is accrued daily. This means I can withdraw my money anytime and don’t have to worry about losing the returns I’ve earned while my money is with the cash management portfolio.

Do take note that although the interest is accrued daily, the returns will be reflected in StashAway Simple’s account monthly.

7. No need to worry about dormant account

Recently, two of my bank accounts became inactive because I didn’t initiate any transactions for a continuous period of 12 months. To reactivate these bank accounts, I had to personally visit the bank and perform a deposit or withdrawal over the counter.

Honestly, I prefer not to go to the bank unless really necessary, especially during a pandemic like now.

With StashAway Simple, I don’t have to worry about inactive or dormant account issues.

StashAway Simple vs Fixed Deposit

Now, let’s have a closer look at the comparison between Stashaway Simple and Fixed Deposit.

To be fair to both, I am comparing StashAway Simple with Maybank’s e-Fixed Deposit. I choose Maybank e-Fixed Deposit (MBB e-FD) because I am using one myself and I am familiar with it.

Also, it is an online Fixed Deposit. So, some of the features are quite similar to StashAway Simple, such as initiating and completing the fixed deposit placement online.

Comparison between StashAway Simple and Fixed Deposit

The table below shows the comparison between StashAway Simple and Fixed Deposit.

| Features | StashAway Simple | Fixed Deposit (MBB e-FD) |

|---|---|---|

| Returns | the projected rate of 2.4% p.a. | Between 1.50% p.a. to 2.10% p.a. |

| Guaranteed returns | No, but the risk is minimal | Yes |

| Capital protection | No, but the risk is minimal | Yes |

| Lock-in period | No | Between 1 month to 60 months |

| Minimum initial deposit | Any amount | RM5,000 for 1 month and RM1,000 for 2 months and above |

| Impact on returns for premature withdrawal | Not affected | Possibility of losing part of the interest* |

| Withdrawal timeline | 3 to 4 business days | Instant |

| Partial withdrawal | Yes | No, only support full withdrawal |

| Auto-deposit feature | Yes | No |

| PIDM protection up to RM250,000 per depositor per bank member | No | Yes |

| Shariah-compliance | Yes (as of January 2024) | The option is available under e-Islamic Fixed Deposit-i |

| Opening of account over the counter | No, everything is completed online | No, as long as an existing MBB2U (Maybank online) customer |

| Service availability | 24/7 | 6 am until 10 pm, daily including public holidays |

*MBB e-FD requires a 30-day withdrawal notice to enjoy 50% of the returns

From the above StashAway Simple vs Fixed Deposit table, it’s clear that there are pros and cons for both StashAway Simple and Fixed Deposit.

All I can say, the choice depends on some of the factors below:

- current economic conditions

- risk preferences

- personal preferences

As for me, due to the current low Fixed Deposit rates, I am highly considering moving a portion of my Fixed Deposit to StashAway Simple.

Who is StashAway Simple suitable for?

Are you wondering whether StashAway Simple is the right cash management solution for you?

Below are some of the ways I believe StashAway Simple would be useful, depending on your preferences and financial goals.

Alternative to fixed deposit

At times like now, where the Fixed Deposit interest rate dropped from about 1.50% p.a. to 2.10% p.a., the StashAway Simple projected rate of 2.4% p.a. looks much more appealing.

Especially when coupled with other benefits such as no platform fees and the flexibility to withdraw at any time without losing the interest earned earlier.

If you are like me, having some Fixed Deposit placement at the bank, I believe you would agree if I said, in the current situation Stashaway Simple is a great alternative to a fixed deposit.

At least until when the pandemic is improved and the economy is growing.

When the time comes, I can compare and decide whether to put my savings in StashAway Simple or move back to Fixed Deposit or probably another better alternative.

Earn interest while saving for a goal

Are you saving for a goal, such as a down payment for a new home? While still hunting around for the right home, why not consider growing your savings using StashAway Simple?

Let’s say you’ve saved RM50,000 as the down payment for a new home. With the projected return of 2.4% p.a., you could be earning RM1,200. And this RM1,200 can buy you a nice dining table set for your new home.

Earn interest while waiting for the right opportunity

Do you have some savings put aside, waiting for the right opportunity? For example, waiting to buy a studio apartment for investment. Or, perhaps waiting for favorable conditions to invest in the StashAway portfolio?

Instead of keeping the money in a conventional savings account, you may consider StashAway Simple cash management to grow your savings.

Simply earn interest with your stash away

I believe we all have some money stashed away somewhere.

For college students (StashAway Simple minimum age is 18 years old), probably you’ve got some savings from:

- part-time jobs as a college student

- pocket money from your parents

- PTPTN study loan or other scholarship

For working adults:

- savings from your monthly income

- year-end bonus

- savings for emergency funds

- income from freelance jobs

Since Stashaway Simple is easy to use with no initial deposit, anyone can just sign up and let their stash away grow with a projected return of 2.4% per annum.

StashAway Simple onboarding procedure

In this Stashaway Simple review, I’ll also include a simple onboarding process.

How to sign-up StashAway Simple?

Signing up for StashAway Simple is really easy. Most importantly, it is free.

You may consider registering for a StashAway account through my StashAway referral link.

Although StashAway Simple is no fees, just in case you want to try out the StashAway general investing, you’ll get 50% fees deducted for 6 months up to RM100,000 invested.

(Do take note to deposit any amount into your StashAway general investing within 30 days of registration to entitle to the 50% discounted fees)

Once you’ve signed up and filled in all related information including a Know Your Customer (KYC) procedure, follow the rest of the instructions and wait for your account activation.

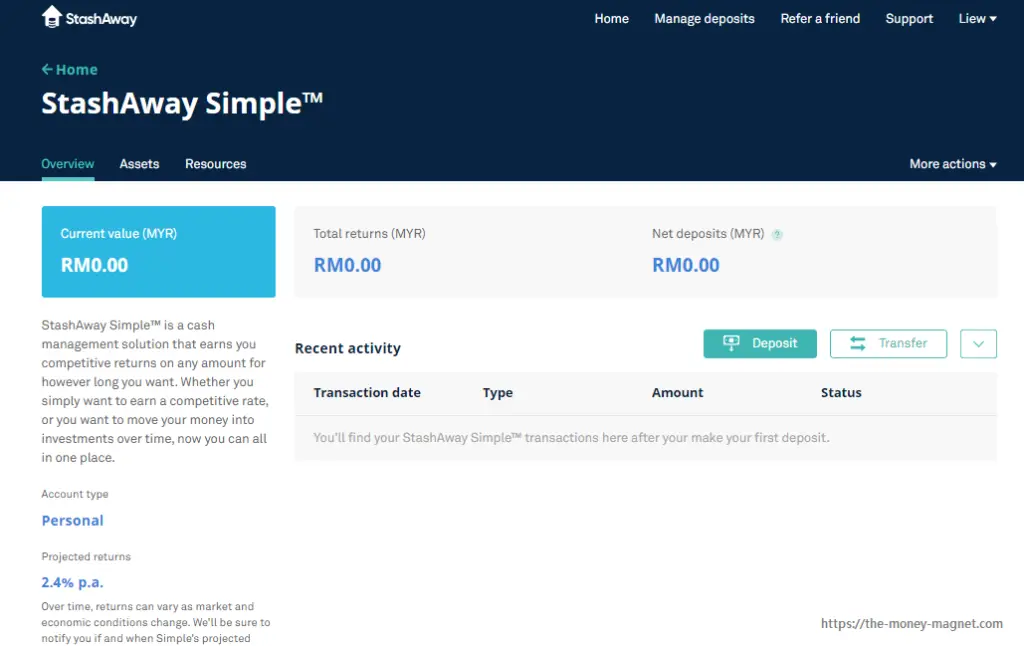

How to deposit to StashAway Simple?

Upon account activation, you may make your first deposit to StashAway Simple.

Firstly, log in to your account and go to the StashAway Simple under Cash Management.

Then, fill in the amount you wish to deposit to the cash management.

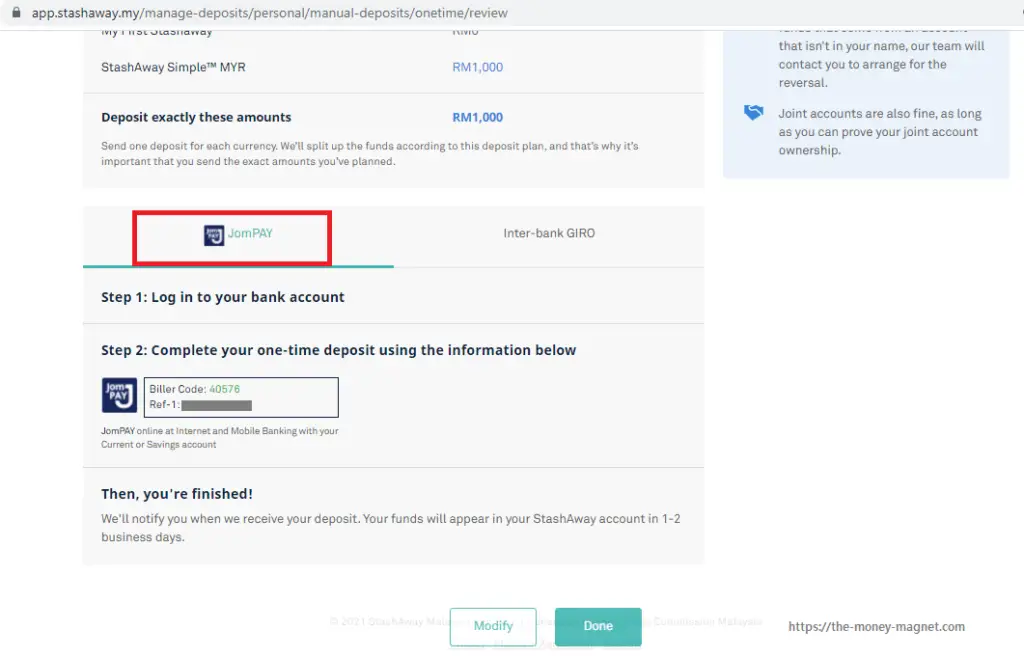

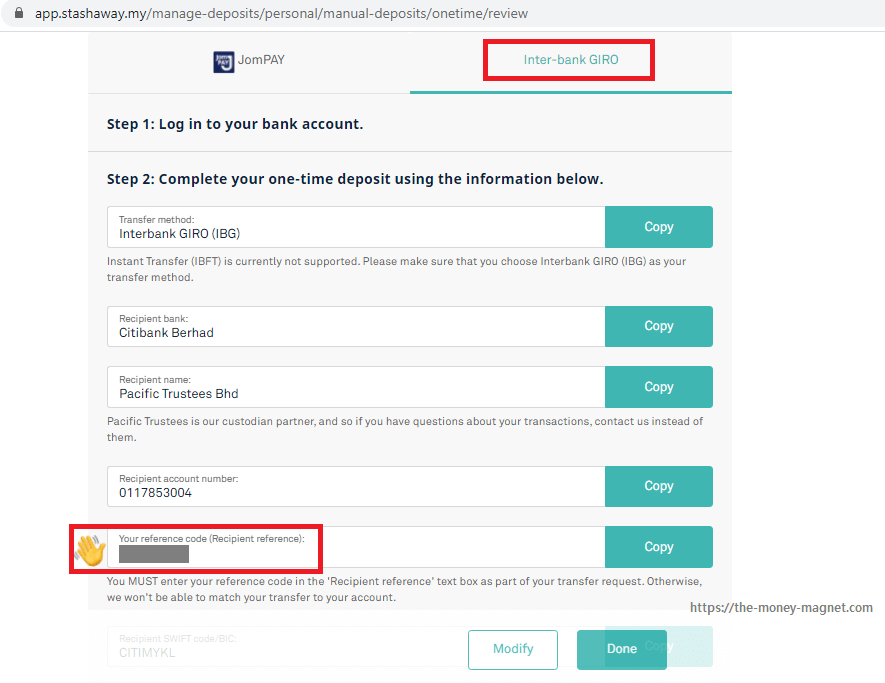

At the time of writing, you can either deposit through JomPAY or Interbank GIRO (IBG).

Deposit through JomPAY

Deposit through Interbank GIRO (IBG)

Personally, I prefer depositing through JomPAY because the procedure is simpler.

Do make sure you take note of the important stuff such as the unique reference code. This is to ensure the deposit is transferred correctly and successfully to your StashAway account.

It might require 2 to 3 business days before the deposit is reflected in your account. Once the deposit is confirmed, they’ll start the process to invest it.

And once invested, I can log in and view my Cash management current value.

From time to time, I do receive StashAway email notifications on the latest update. So, I don’t have to worry about my deposits.

StashAway Simple returns (2024)

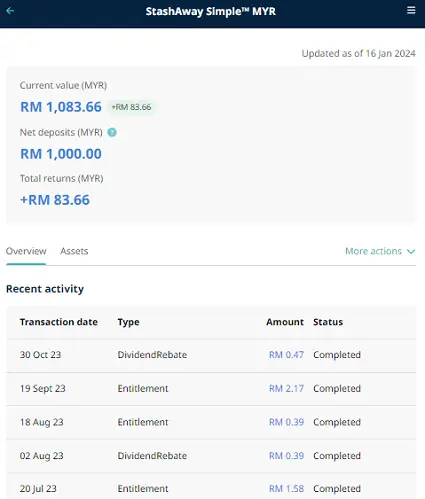

As mentioned earlier, I’ll include my StashAway Simple performance in this StashAway Simple review.

Below is a screenshot of my latest StashAway Simple returns.

The total return is RM83.66 for a net deposit of RM1,000 within about 31 months. Overall, not bad compared with Fixed Deposits.

I shall update my StashAway Simple performance from time to time.

Final thoughts

With the above StashAway Simple review, I hope you find my sharing beneficial.

If you wish to try out StashAway Simple, do sign up through my StashAway referral link. Through the promo link, you’ll enjoy 50% of fees for 6 months for investments up to RM100,000 should you decide to invest in StashAway general investing.

Take note to deposit any amount to your StashAway general investing within 30 days of registration to enjoy the 50% discounted fees.

And if you are wondering what are the differences between StashAway and StashAway Simple, you may read my other sharing on StashAway vs StashAway Simple.

Do you have any other questions related to my StashAway Simple review? Please leave your questions or comments below.

Image Credits

Featured image by RoboAdvisor from Pixabay

All Screenshots were taken by the author